Introduction

FinTech leaders and neo bank operators face a distinct pressure: they must move at startup speed while managing institutional-grade risk, compliance, and security. The firms pulling ahead aren't necessarily those with the largest budgets — they're the ones that have moved AI from experimental project to core infrastructure. Financial services firms spent $35 billion on AI in 2023 and are projected to reach $97 billion by 2027 — a 177% increase that signals AI has crossed from pilot-stage curiosity to mission-critical capability.

What that shift looks like in practice — and how to avoid the common trap of AI builds that work in demos but fail in production — is what this piece breaks down.

Key Takeaways

- AI adoption in FinTech and neo banking has moved from experimental to operational. Fraud detection, credit decisioning, compliance automation, and personalized banking now run on it.

- The right AI consulting partner combines deep financial domain expertise, compliance-first architecture, and production-grade delivery.

- Neo banks benefit from AI-native infrastructure— built to compete with legacy institutions without the overhead of traditional systems

- 74% of GenAI pioneers in financial services report ROI exceeding 10%, yet 95% of pilots never reach measurable P&L impact. Execution quality is what separates the two.

Why AI Is No Longer Optional for FinTech & Neo Banks

Financial services have reached an inflection point. Customer expectations for real-time, personalized, seamless financial experiences now exceed what rule-based or manual systems can deliver. AI is what closes that gap.

The convergence of mobile-first banking, open banking APIs, and rising digital transaction volumes makes adoption both an opportunity and a necessity. Open Banking API calls will grow 427%, from 137 billion in 2025 to 720 billion by 2029. Manual processing at that scale is physically impossible.

Neo banks specifically use AI as a core competitive weapon. They lack the branch networks and brand legacy of traditional banks, so AI-powered personalization, smart onboarding, and automated support become their primary differentiators against incumbents. Where legacy banks wrestle with decades of technical debt and fragmented systems, neo banks can architect AI-native infrastructure from the ground up, provided they choose partners who understand financial services compliance and not just machine learning theory.

AI also delivers measurable operational efficiency gains across lending, compliance, and customer support. The numbers are concrete:

- Loan and compliance turnaround times drop significantly with automated review workflows

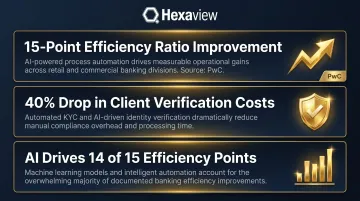

- PwC reports a 15-percentage-point improvement in bank efficiency ratios from AI adoption, with AI-driven operations contributing 14 of those points

- Client verification costs fell 40% at one institution after deploying AI-driven onboarding tools

In an industry where efficiency ratios directly determine competitiveness, a 15-point swing is structural, not incremental.

The regulatory environment is also accelerating AI adoption, not slowing it. Explainable AI models, automated audit trails, and real-time transaction monitoring help firms meet AML, KYC, and data privacy requirements more consistently than manual processes. The CFPB's 2023 guidance requires lenders to provide specific reasons for AI-driven credit denials. Firms that design for explainability from day one meet that requirement while demonstrating compliance rigor that manual processes can't match.

Firms that delay AI adoption cede ground to digitally native competitors and AI-first neo banks. 31% of financial institutions currently deploy generative AI for external use cases, and that share is climbing. Early movers are building advantages in customer experience, operational cost structure, and risk management that will be difficult for followers to reverse.

High-Impact AI Use Cases in FinTech & Neo Banking

AI delivers measurable ROI across FinTech functions—but the highest-impact applications differ significantly by use case. Here's where leading institutions are seeing results worth prioritizing.

Fraud Detection & AML Compliance Automation

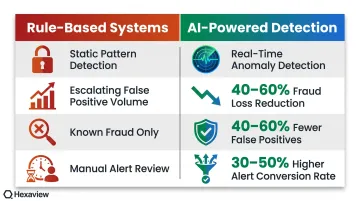

AI-powered fraud detection systems monitor transactions in real time, identify anomalous patterns across thousands of variables simultaneously, and flag suspicious activity before losses occur—unlike rule-based systems that only catch known fraud patterns. 90% of financial institutions now use AI to fight fraud, with 39% reporting 40-60% fraud loss reductions and 34% reporting 40-60% reductions in false positives.

The false positive problem illustrates why rule-based systems fail: static rules generate escalating alert volumes as transaction complexity grows. AI addresses this through adaptive pattern recognition. Automated AML monitoring reduces the manual burden on compliance teams while improving detection accuracy—one study found AI-based filtering increases conversion from fraud alerts to actionable cases by 30-50%.

AI-Driven Credit Scoring & Underwriting

Machine learning models go beyond traditional FICO-based credit scoring by incorporating alternative data signals—transaction history, payment behavior, utility records—to assess creditworthiness more accurately and inclusively. Alternative data can accurately score more than 50% of previously unscorable credit applicants, and adding alternative data increases predictive value by 5-20% over traditional-data-only models.

A TransUnion study found that including rental payments boosted average credit scores by 60 points. A US GAO analysis found 17% of previously ineligible mortgage applications could have qualified if rental history were considered. For neo banks serving customers without extensive credit histories, AI-driven underwriting isn't just an efficiency play—it's a market expansion strategy.

Personalized Banking & Wealth Management

The operational gains are concrete: one bank cut investment brief production time by 90%—from nine hours to 30 minutes—using AI-powered synthesis. AI also automates SARs, model documentation, and validation reports, while continuously monitoring model performance and generating alerts when metrics drift outside tolerance levels.

Automated KYC & Smart Customer Operations

AI accelerates and automates customer identity verification—document scanning, biometric checks, sanctions screening—as part of onboarding, reducing drop-off rates while maintaining compliance. Financial services KYC/KYB spending will reach $30.5 billion by 2030, up 40% from 2025, driven by AI-driven fraud and synthetic identities.

AI-powered virtual assistants handle routine customer queries at scale, freeing human agents for complex issues. EY reports that AI automation in compliance processes achieves regulatory reporting accuracy rates up to 98%, and AI-based merchant onboarding reduces approval time by 70%.

Why Building AI for Financial Services Is Harder Than It Looks

AI development for FinTech isn't just a technical challenge—it's a domain challenge. A team that builds excellent AI for e-commerce may lack the financial domain knowledge to understand what makes a credit model biased, how a compliance audit trail needs to be structured, or what "explainability" means for a regulator. Domain fluency and technical depth must coexist, and that combination is rare.

The compliance and security complexity specific to financial AI raises the bar from day one. Every system must meet a demanding baseline:

- Models must be fully auditable with documented decision logic

- Data must be encrypted, access-controlled, and scoped to regulatory requirements

- Standards like SOC 2, PCI-DSS, and GDPR/CCPA apply from the first deployment

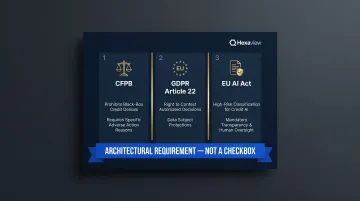

The CFPB explicitly prohibits "black box" defenses for credit denials, and the EU AI Act classifies credit scoring AI as "high-risk," requiring transparency and human oversight. These are architectural requirements baked into every design decision — not compliance checkboxes added at the end.

The production gap is where most AI consulting firms fail. 95% of generative AI pilots fail to deliver measurable P&L impact, and the gap between proof-of-concept and enterprise rollout is where models break down. Many consulting firms deliver prototypes that were never designed for integration with legacy banking systems, real-time data pipelines, or enterprise-grade cloud infrastructure.

Production-readiness is the right benchmark — not model accuracy alone. Vendor-built solutions succeed at 67% versus 22% for internal builds, suggesting that specialized domain expertise and deployment patterns matter more than engineering headcount. The firms that close the production gap treat MLOps, model monitoring, drift detection, and core banking integration as foundational requirements from day one.

What to Look for in an AI Development & Consulting Partner

Choosing an AI partner is a strategic decision that goes beyond technology stack evaluation. The right criteria combine domain depth, delivery philosophy, and long-term support.

Financial Domain Expertise

The most reliable signal of a capable AI partner is demonstrated experience in financial services workflows—credit, payments, compliance, wealth management, capital markets—not just general AI competency. A partner with 10+ years of capital market and wealth management experience serving institutional-grade financial firms is fundamentally different from a generalist software firm.

Hexaview's decade-plus focus on FinTech, wealth management, and capital markets—serving clients like LPL Financial and Addepar—reflects this depth. Domain expertise means understanding not just how to build a fraud detection model, but how that model integrates with AML workflows, what regulators will ask during audits, and which alternative data sources introduce bias risk.

Security & Compliance Certifications

Certifications matter beyond marketing. SOC 2 Type 2, ISO 27001, and cloud partnership credentials such as AWS Select Tier signal that a firm has institutionalized security practices and can be trusted with sensitive financial data. Financial institutions should require evidence of these certifications—not just claims—before engaging any AI partner.

These credentials confirm that security controls, data handling procedures, and compliance frameworks are audited and verified—not simply written down in a policy document.

Production-Grade AI Delivery

Differentiate between firms that deliver AI experiments and those that build production systems. Look for partners with:

- MLOps capabilities and model monitoring infrastructure

- Integration experience with core banking systems and financial APIs

- A track record of moving from pilot to enterprise rollout without failure

Ask specific questions before committing:

- How do you handle model drift?

- What monitoring infrastructure do you deploy post-launch?

- How do you integrate with legacy core banking platforms?

- How do you ensure consistent performance under production load?

The answers quickly reveal whether the firm understands production AI or has only built prototypes.

Explainability & Audit Readiness

Financial regulators increasingly require AI models used in lending, compliance, and risk to be explainable—meaning the system can articulate why a decision was made in terms a compliance officer or regulator can evaluate. Partners that can't design for explainability create downstream regulatory exposure.

These are current legal obligations—not future hypotheticals:

- GDPR Article 22 grants data subjects the right to contest automated decisions

- CFPB guidance requires specific adverse action reasons for credit decisions

- EU AI Act mandates conformity assessments for high-risk AI systems

AI partners must build explainability infrastructure from the start. Retrofitting it after regulators ask questions is expensive and often incomplete.

Engagement Model & Long-Term Support

AI in FinTech isn't a "build and hand off" engagement—models drift, regulations change, and financial products evolve. Evaluate whether the partner offers ongoing model monitoring, retraining, and strategic consulting to keep the AI system performing over time.

The best partnerships include post-deployment support: performance monitoring dashboards, automated drift detection, scheduled retraining protocols, and access to domain experts who understand how regulatory changes affect model design. Firms that treat AI deployment as the end of the engagement rather than the beginning create technical debt that compounds over time.

AI Trends Reshaping FinTech & Neo Banks in the Near Future

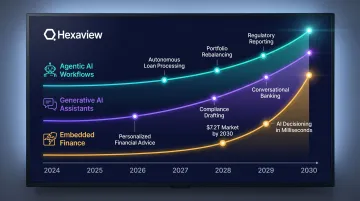

Agentic AI and autonomous financial workflows represent the next wave of FinTech efficiency gains. These are AI systems that don't just assist — they independently execute multi-step financial processes with human oversight at defined checkpoints:

- End-to-end loan processing

- Automated regulatory reporting

- Real-time portfolio rebalancing

23% of consumers already use generative AI for financial tasks at least monthly, and McKinsey projects that within 3-5 years, AI agents could autonomously optimize credit choices, payment routing, and rewards usage.

The disintermediation risk is real: if AI agents sit at the decision layer between consumers and financial products, they shift competitive advantage from product manufacturers (banks) to agent operators (technology platforms). This mirrors what happened in travel, where aggregator platforms captured customer relationships from airlines and hotels — and banks that wait risk the same outcome.

Generative AI is enabling a new class of financial assistant that can synthesize financial data, generate personalized advice narratives, draft compliance reports, or answer complex customer questions conversationally. Unlike earlier AI tools limited to pattern recognition, these systems generate explanations, summaries, and recommendations that previously required human financial analysts — reshaping both front-office experience and back-office workflows.

Those same generative capabilities are powering the next shift: embedded finance. The embedded finance market is expected to reach $7.2 trillion by 2030, with AI driving the invisible financial infrastructure embedded into e-commerce, payroll, and HR platforms.

Firms building or powering that infrastructure need real-time AI decisioning at scale — executing credit decisions, fraud checks, and compliance verifications in milliseconds. Across millions of daily transactions, latency is not an option.

Frequently Asked Questions

Is AI taking over financial analysts?

No—AI augments rather than replaces financial analysts. It handles data-heavy, repetitive analysis tasks like pattern detection, report generation, and portfolio monitoring, freeing analysts to focus on strategic interpretation, client relationships, and complex judgment calls that require domain experience and context.

What AI services do FinTech companies need most?

The highest-demand AI services are fraud detection and AML automation, AI-powered credit scoring, automated KYC/onboarding, predictive risk analytics, and personalized financial recommendation engines. Priorities depend on whether the firm is a lender, neo bank, wealth platform, or payments provider.

How long does it take to implement AI solutions for a neo bank?

A focused pilot (fraud detection model or automated KYC flow) typically takes 8-16 weeks to deploy. Enterprise-grade multi-system AI platforms can take 4-9 months, depending on data readiness, integration complexity, and compliance requirements.

What compliance certifications should an AI consulting firm have for FinTech work?

Look for SOC 2 Type 2 (data security and availability), ISO 27001 (information security management), and relevant cloud certifications such as AWS Select Tier Service Partner status. Verify demonstrated familiarity with PCI-DSS, AML/KYC frameworks, and applicable data privacy regulations like GDPR and CCPA.

How is AI development different for neo banks vs. traditional banks?

Neo banks typically lack legacy system constraints, making AI-native architecture easier to implement from scratch, but they face accelerated compliance timelines and must scale rapidly. Traditional banks face integration complexity but bring existing data assets and established regulatory relationships.

What is the ROI of AI development for FinTech companies?

ROI varies by use case. Fraud detection reduces loss exposure directly: 39% of institutions report 40-60% fraud loss reductions. AI underwriting cuts processing costs and improves approval accuracy. Automated compliance reduces labor-intensive manual reviews. 74% of GenAI pioneers estimate ROI exceeding 10%, with McKinsey projecting $200-340 billion in annual banking value from AI.