Introduction

Wealth managers and neo banks face mounting pressure from three converging forces: clients who expect real-time, hyper-personalized service, compliance burdens that grow exponentially with each regulatory cycle, and margin compression that makes manual operations economically unsustainable. More than 50% of digital bank account applications are abandoned mid-process, compliance costs have reached $61 billion annually in North America alone, and the industry faces a projected shortage of 90,000 to 110,000 advisors by 2034. Traditional automation—rigid RPA scripts and reactive chatbots—can't solve these problems.

Agentic AI workflow automation represents a fundamentally different approach. Unlike RPA that follows predetermined scripts or chatbot-era AI that responds to prompts, agentic AI systems autonomously plan, execute, and adapt multi-step financial workflows.

These systems orchestrate specialized agents — compliance monitors, identity verification agents, portfolio rebalancing agents — that coordinate across tools and data sources, make judgment calls within defined boundaries, and escalate only genuine exceptions to humans.

2026 marks a shift from experimentation to production. Global AI spending will hit $2.52 trillion this year — a 44% year-over-year increase — nearly 50% of tier-one banks are deploying AI agents for back-office operations, and 78% of wealth firms are actively exploring agentic implementations. Multi-agent orchestration platforms, regulatory sandboxes in the EU, and standards like the Agent2Agent Protocol have removed the technical and compliance barriers that stalled earlier deployments.

Institutions that move now — with clear governance frameworks — stand to gain measurable advantages in processing speed, compliance accuracy, and client retention before this shift becomes table stakes.

Key Takeaways

- Agentic AI moved from enterprise pilots to live production in 2026, with multi-agent systems replacing manual handoffs in KYC, compliance, advisory, and fraud detection

- Five dominant trends: autonomous KYC onboarding, continuous compliance surveillance, AI-augmented advisory, proactive conversational agents, and real-time fraud pipelines

- Neo banks lead adoption due to API-first architectures — traditional wealth managers that move now will close that gap before it becomes structural

- Regulatory complexity accelerates adoption rather than slowing it—compliance-by-design is now core to agentic architecture

- Define agent decision boundaries and governance frameworks before scaling — retrofitting guardrails after deployment costs significantly more in time and risk

Agentic KYC and Client Onboarding Automation

Digital bank onboarding remains one of the highest-friction processes in financial services. More than 50% of applicants abandon a digital account application — with rates climbing to 60-80% depending on verification steps — and nearly 20% drop out at just five questions.

How Multi-Agent KYC Pipelines Work

Agentic KYC systems deploy specialized agents that handle discrete steps in parallel rather than sequential manual handoffs:

- Document extraction agents pull data from passports, utility bills, and financial statements using intelligent document processing (IDP)

- Identity verification agents cross-reference extracted data against sanctions lists, credit bureaus, and watchlists simultaneously

- Risk scoring agents evaluate application data against AML rules and behavioral models

- Account provisioning agents create accounts, set permissions, and trigger onboarding communications

- Escalation agents route genuine exceptions (document quality issues, sanctions hits) to human reviewers with full context

Together, these agents compress onboarding from days to minutes. Institutions that defer non-essential steps until after account activation have seen increases in new accounts of up to 150%. AI-powered personalization in banking can reduce customer acquisition costs by up to 50%.

Reducing perceived friction through intelligent pre-filling and parallel verification lets institutions recapture lost conversions without weakening AML and sanctions controls. For neo banks, faster onboarding is a direct competitive lever. For traditional institutions, it's foundational infrastructure that's increasingly hard to defer.

Autonomous Compliance and Regulatory Surveillance Agents

The compliance cost burden alone is forcing wealth management firms and neo banks to rethink manual review entirely. Annual compliance costs total $61 billion in the United States and Canada, with 99% of financial institutions reporting cost increases. SAR filing volumes grew from 4.3 million in FY2022 to 4.7 million in FY2024, averaging 12,870 daily filings. Alert volumes continue climbing: 87% of small organizations and 83% of mid-to-large organizations report increases in screening alerts.

How Autonomous Compliance Agents Operate

That volume makes periodic manual review structurally unworkable. Wealth management firms and neo banks now deploy persistent compliance agents that continuously monitor transactions, communications, and portfolio actions:

- Transaction monitoring agents analyze payment streams against AML rules in real time, correlating patterns across accounts and geographies

- Communications surveillance agents scan advisor-client interactions for conduct violations under FINRA/SEC standards

- KYC refresh agents trigger re-verification workflows when risk signals appear (address changes, transaction anomalies, adverse media)

- Regulatory intelligence agents ingest updated guidance from regulatory APIs and flag rule changes requiring workflow adjustments

- SAR drafting agents auto-generate suspicious activity report drafts with supporting evidence for human review

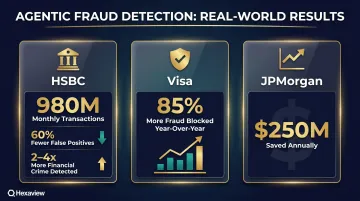

Case study: HSBC processes approximately 980 million transactions monthly through its Dynamic Risk Assessment system, achieving 60% fewer false positives while detecting 2-4x more financial crime. Analysis time compressed from several weeks to a few days.

Regulatory context: By August 2026, all EU Member States must establish AI regulatory sandboxes under the EU AI Act, with AI systems in AML, fraud detection, and KYC classified as high-risk. For firms already building compliant agent architectures, the sandbox structure gives compliance teams a defined testing environment — reducing the legal ambiguity that previously slowed deployment.

Hyper-Personalized Advisory and Multi-Agent Portfolio Management

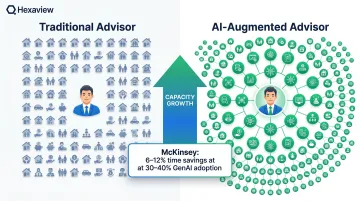

The US wealth management industry is heading toward a structural advisor shortage of 90,000 to 110,000 by 2034, driven largely by 110,000 retirements — roughly 38% of today's workforce. The constraint is already visible: advisors currently manage 88–98 households on average, leaving almost no bandwidth for business development or proactive client engagement.

Multi-Agent Advisory Architecture

Wealth management firms are orchestrating multiple specialized agents that collaborate to generate personalized recommendations and execute rule-based actions:

Specialized agent types:

- Market data agents monitor real-time price movements and market dislocations

- Risk profiling agents track client circumstances (life events, liquidity needs, risk tolerance shifts)

- ESG scoring agents evaluate portfolio holdings against sustainability criteria

- Tax optimization agents identify tax-loss harvesting triggers and wash sale constraints

- Rebalancing agents execute approved portfolio adjustments within drift tolerances

These agents work simultaneously, triggering recommendations when multiple conditions converge—such as a tax-loss harvesting opportunity during a market dip for a client approaching retirement.

The capacity math is compelling. McKinsey projects 6–12% time savings from generative AI at 30–40% adoption rates. In practice, an advisor managing 150 relationships can — with agentic augmentation — deliver personalized touchpoints across 500+ clients.

Enterprise deployments confirm the economics. JPMorgan rolled out its LLM Suite to 200,000+ employees within eight months, reporting 30–40% efficiency gains. Its Connect Coach tool gives Private Bank advisors AI-generated client insights on demand. The bank now estimates up to $1.5 billion in annual value from AI initiatives across the firm.

For firms like LPL Financial and Addepar — both part of Hexaview's client base — this shift is already operational. Multi-agent systems are expanding advisor capacity without proportional headcount increases, a model that will become the baseline expectation across enterprise wealth management by 2026.

Conversational Finance Agents and Embedded Banking Intelligence

Unlike static chatbots that wait for user queries, proactive conversational agents initiate engagement based on predicted needs. Neo banks and digital wealth platforms embed these agents into mobile apps, where they surface spending anomalies, savings opportunities, upcoming bills, and investment nudges using real-time account data.

Proactive vs. Reactive: The Key Differentiator

Agentic conversational systems go well beyond answering questions. They:

- Maintain persistent memory of user financial history, goals, and past interactions

- Contextualize advice over time rather than treating each interaction as isolated

- Initiate conversations when patterns trigger engagement rules (unusual spending, goal milestone)

- Adapt tone and recommendations based on user preferences and engagement history

Quantified impact:

- Banks implementing AI-driven personalization see customer retention increases of as much as 15%

- Cross-sell success rates improve by 30%

- Real-time personalization delivers 3x higher click-through rates versus batch-processed recommendations

Only 14% of banks have achieved predictive personalization at scale, yet AI personalization could add $340 billion in annual value to the banking industry. For institutions still running batch-processed recommendations, that gap is where their competitors are already gaining ground.

Real-Time Fraud Detection and AML Agentic Pipelines

Financial fraud escalated sharply in 2024. US consumers lost more than $12.5 billion to fraud, a 25% increase over 2023. The loss incidence rate jumped from 27% in 2023 to 38% in 2024, meaning more reported fraud resulted in actual monetary loss.

Agentic Fraud Pipelines Replace Batch Rules

Continuous multi-agent pipelines monitor transaction streams in real time, correlating signals across multiple dimensions:

- Behavioral baseline agents track normal spending patterns and flag deviations

- Network graph agents correlate activity across accounts, geographies, and channels simultaneously

- Watchlist screening agents cross-reference transactions against sanctions lists and adverse media

- Escalation agents dynamically route high-confidence alerts to investigators or auto-block suspicious transactions pending review

Real-world performance:

- HSBC's system processes 980 million transactions monthly with 60% fewer false positives and 2-4x more detected financial crime

- Visa's AI/ML systems blocked nearly 85% more fraud compared to the prior year

- JPMorgan's fraud prevention system saves $250 million annually

Results like these have caught regulators' attention. Real-time monitoring is now treated as a compliance expectation, not a best practice. For neo banks handling high transaction volumes with lean operations teams, agentic fraud detection delivers on two fronts: operational efficiency and regulatory necessity.

What's Driving These Agentic AI Trends in Wealth Management and Neo Banking

These trends aren't happening by accident. In 2026, five structural forces are converging to make agentic AI adoption both viable and urgent for wealth managers and neo banks.

Technology Advances Enable Production-Scale Deployment

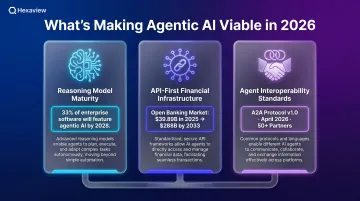

Three infrastructure shifts have moved agentic AI from prototype to production:

- Reasoning model maturity: Longer context windows, better tool use, and improved planning make multi-step financial workflows feasible. By 2028, 33% of enterprise software will feature agentic AI—up from less than 1% in 2024.

- API-first financial infrastructure: Open banking mandates and core banking modernization provide the integration layer agentic systems need. The open banking market hit $39.89 billion in 2025 and is projected to reach $288.36 billion by 2033.

- Agent interoperability standards: The Agent2Agent Protocol (A2A) reached v1.0 in April 2026, letting AI agents discover each other's capabilities and coordinate across vendors. Over 50 partners—including PayPal, Intuit, and Salesforce—contributed to the standard.

Market Demand and Generational Expectations

Digital-native clients expect personalized, proactive financial experiences—and the data reflects that expectation. 71% of consumers expect personalized interactions, with 76% frustrated when they don't get them. Nearly 70% of millennials and Gen Z have already authorized banks to share their data with third parties—comfort levels that make agentic personalization a natural next step rather than a hard sell.

Cost Pressures and Efficiency Needs

Wealth managers face fee compression: by 2026, 83% of financial advisors expect to charge less than 1% for clients with more than $5M in assets, with average fees for $10M+ clients dropping to approximately 66 basis points. Neo banks must achieve profitability with lean teams. Agentic automation lets both serve more clients at higher quality—without a corresponding increase in headcount.

Regulatory and Compliance Pressure

Growing AML, KYC, ESG disclosure, and suitability requirements create unsustainable manual compliance loads. 79% of organizations saw technology cost increases for KYC software. Agentic systems handle continuous rule monitoring at scale, with SOC 2 Type 2-certified implementation partners like Hexaview ensuring these systems meet security and auditability standards.

Competitive Dynamics

Neo bank entrants with clean-sheet AI-native stacks outpace legacy institutions on onboarding speed and personalization. The performance delta is measurable: high-performing firms onboard clients in 8.5 weeks versus 10.3 weeks at other firms. That 1.8-week gap translates directly into client acquisition and retention—a margin incumbents can't afford to cede.

How These Trends Are Impacting Wealth Management and Neo Banks

Operational Impact

The operational shifts are measurable and accelerating:

- Compliance review cycles are shortening as agentic systems flag anomalies in real time

- Client onboarding is compressing from days to minutes through automated KYC and document workflows

- Portfolio monitoring is moving from periodic snapshots to continuous, always-on surveillance

HSBC compressed transaction analysis time from several weeks to a few days. JPMorgan achieved 30-40% efficiency gains across 200,000+ employees. Institutions that deferred non-essential onboarding steps opened up to 150% more accounts.

Business Impact

Wealth management firms are re-allocating advisor time toward high-value relationship and planning work, while agents handle execution and monitoring. Neo banks are treating agentic capabilities as a core product differentiator — a structural advantage that's harder for incumbents to replicate than a feature update. Investment in agentic AI infrastructure is now appearing as a line item in fintech capex planning, with global AI spending forecast at $2.52 trillion in 2026.

Workforce Impact

The workforce shift is less about displacement and more about redefinition. Compliance analysts, portfolio operations staff, and customer support agents are moving into AI supervision and exception-handling roles — where human judgment remains the critical check on automated decisions. New job categories like agent workflow designer and financial AI auditor are emerging in response.

Firms that invest in upskilling early are seeing faster adoption rates and fewer implementation setbacks than those treating workforce transition as an afterthought.

Future Signals for Agentic AI in Wealth Management and Neo Banking

What's already live in 2025 is the foundation. The signals emerging from protocol releases, regulatory mandates, and Gartner research point to a materially different operating model for wealth management and neo banking by 2028.

Agent-to-Agent Communication Protocols

The A2A protocol's progression to v1.0 in April 2026 enables fully orchestrated financial ecosystems where a client's tax agent, investment agent, and banking agent coordinate seamlessly across institutions without human-initiated handoffs. This multi-vendor interoperability removes the lock-in barrier that previously constrained agentic adoption.

Regulatory Sandboxes for Autonomous Decision-Making

By August 2026, all EU Member States must establish AI regulatory sandboxes under the EU AI Act. As these frameworks solidify, production deployment of higher-autonomy agents will accelerate. Institutions participating in sandboxes gain early clarity on governance requirements, positioning them to scale faster than competitors waiting for final regulations.

Agentic Wealth Operating Systems

By 2027-2028, layered multi-agent architectures will handle all client lifecycle events—onboarding, advisory, compliance, reporting—through a unified agentic platform. Gartner predicts at least 15% of day-to-day work decisions will be made autonomously via agentic AI by 2028, up from 0% in 2024. Firms building agent-ready data infrastructure and governance frameworks now are buying time-to-scale advantages that late movers won't easily close.

Risk factor: Gartner warns that over 40% of agentic AI projects will be canceled by end of 2027 due to escalating costs, unclear business value, or inadequate risk controls. Disciplined vendor selection and phased deployment with clear ROI gates are critical.

Conclusion

Agentic AI workflow automation has moved from pilot to production across wealth management and neo banking in 2026. Financial institutions are using it to onboard clients faster, compress compliance costs, scale personalized advice, and tighten fraud detection simultaneously.

The business case is concrete: onboarding abandonment drops by half, advisors manage 3x more clients without sacrificing personalization, and fraud detection improves while false positives fall sharply.

Firms that adopt early, with clearly defined governance and agent decision boundaries, will compound advantages in speed, cost, and client experience over those still iterating on pilots. The competitive window is narrowing: 95% of wealth firms have scaled GenAI, 78% are exploring agentic AI, and nearly 50% of tier-one banks are deploying agents in production. The question is no longer whether to deploy agentic systems, but how to do so with the governance rigor that separates transformative adoption from costly experimentation.

Choosing the right implementation partner matters as much as the technology itself. A partner with deep financial domain knowledge and proven AI engineering capability shortens the path from strategy to production deployment. Hexaview brings over a decade of wealth management and capital markets experience, Agentforce-powered automation, and SOC 2 Type 2 certification to that work — making it a practical choice for firms ready to move beyond the pilot stage and build AI infrastructure that holds up under regulatory scrutiny.

Frequently Asked Questions

What exactly is agentic AI workflow automation in wealth management?

Agentic AI workflow automation refers to autonomous AI systems that plan and execute multi-step financial processes—such as portfolio rebalancing, compliance checks, or client onboarding—without requiring step-by-step human instruction. Unlike traditional RPA or chatbots, these systems reason, adapt to exceptions, and coordinate across tools.

How are neo banks using agentic AI differently from traditional banks?

Neo banks, with API-first cloud-native stacks, can deploy agentic pipelines faster and across the full customer lifecycle. Traditional banks face legacy system integration challenges that require careful orchestration design, though those that invest in agent-ready infrastructure are closing the gap.

What compliance and regulatory risks come with deploying AI agents in financial services?

Key risks include:

- Explainability: Autonomous decisions must be traceable and auditable

- Data privacy: Agents must operate within financial regulatory boundaries

- Governance: Human-in-the-loop checkpoints and role-based access controls are required

SOC 2-certified deployment practices provide the audit trail infrastructure most regulated firms require.

What is the difference between RPA and agentic AI workflows in banking?

RPA automates rule-based, deterministic tasks like data entry. Agentic AI handles judgment-intensive, multi-step workflows—reasoning through exceptions, adapting in real time, and coordinating across tools—making it suitable for compliance surveillance, advisory, and fraud detection.

How can a wealth management firm begin implementing agentic AI without disrupting existing operations?

Start with monitoring-only agents on a high-friction workflow like compliance review. Define clear decision boundaries and escalation rules, then validate against existing processes before expanding execution authority. Phased rollout with clear ROI milestones minimizes disruption while building organizational confidence.

Will agentic AI replace human financial advisors or compliance officers?

Agentic AI handles monitoring, execution, and routine analysis—freeing advisors to focus on relationships, strategy, and complex judgment. Compliance officers shift toward AI oversight and exception resolution, managing higher case volumes with greater consistency.