Introduction

Generative AI has crossed the inflection point in financial services. What began as cautious pilots has become full-scale production deployment — and FinTech firms and Neo Banks are under pressure from every direction.

Customers expect personalized, instant experiences. Operating margins remain thin. Regulatory scrutiny intensifies across jurisdictions. For organizations in this space, GenAI is no longer optional infrastructure — it's how the work gets done.

This post examines what GenAI means specifically for FinTech and Neo Banking organizations, the highest-impact use cases, Neo Bank-specific applications, implementation challenges, and what to evaluate when selecting a GenAI consulting partner.

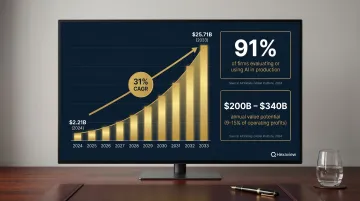

The numbers reflect what's already happening on the ground. Grand View Research projects the global generative AI in financial services market will expand from $2.21 billion in 2024 to $25.71 billion by 2033, representing a 31% CAGR. That growth is driven by measurable deployment across fraud detection, credit risk, compliance automation, and customer engagement workflows.

Key Takeaways

- GenAI reshapes FinTech and Neo Banking through fraud detection, credit risk modeling, regulatory compliance automation, and hyper-personalized customer engagement

- Neo Banks build AI-native financial products from day one on greenfield architectures, bypassing legacy system constraints

- Successful GenAI adoption requires compliance-first design, governed data foundations, and deep financial domain expertise

- Measurable ROI includes reduced fraud losses, accelerated onboarding, lower service costs, and improved credit decisioning accuracy

- Vet GenAI partners for verifiable financial domain experience and security certifications (SOC 2, ISO) before engaging

What Generative AI Actually Means for FinTech and Neo Banks

Generative AI differs fundamentally from traditional machine learning. Where conventional ML classifies or predicts from existing data, GenAI creates—new text, synthetic datasets, decision pathways, code, and personalized experiences. This capability makes GenAI uniquely powerful for customer-facing workflows and compliance-heavy operations.

Traditional banks and established FinTechs must layer GenAI onto existing infrastructure through APIs and middleware. Neo Banks, unburdened by legacy core banking systems, design GenAI-native products from inception—embedding AI into onboarding, credit decisioning, and personalization at the product architecture level.

The adoption shift is measurable. NVIDIA's 2024 financial services survey found that 91% of financial services firms are evaluating or already using AI in production. By 2026, 61% were actively using or assessing generative AI specifically—a 52% year-over-year increase. Firms still in evaluation mode are increasingly the exception, not the rule.

That scale of adoption reflects real financial upside. McKinsey estimates GenAI could deliver $200 billion to $340 billion in annual value to the banking sector—equivalent to 9–15% of operating profits—primarily through productivity gains in customer engagement, compliance, and software engineering.

Top GenAI Use Cases for FinTech Companies

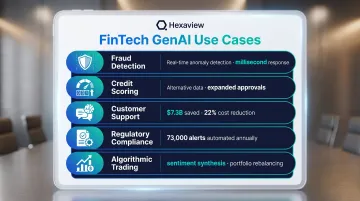

Fraud Detection and Real-Time Risk Monitoring

GenAI models surpass rule-based fraud detection by identifying novel, unseen patterns in transaction behavior. Unlike traditional systems that flag known fraud signatures, GenAI uses anomaly detection and synthetic fraud scenario generation to catch emerging threats before they scale.

The cost case is clear. TransUnion reports that US companies lost 9.8% of revenue to fraud in H1 2025, with global fraud losses reaching $534 billion. The FTC logged $12.5 billion in US consumer fraud losses in 2024 alone, a 25% year-over-year increase.

GenAI reduces false positives—critical for maintaining customer trust—and accelerates detection cycles from hours to milliseconds. FinTechs deploying GenAI fraud systems report faster threat identification and lower operational costs from manual review reduction.

Credit Scoring and Lending Decisioning

GenAI expands credit evaluation beyond traditional bureau data by incorporating behavioral signals, spending patterns, and alternative data sources. This makes lending more accurate and accessible, particularly for FinTechs serving underbanked populations.

Updated CFPB data from June 2025 estimates approximately 7 million US adults (2.7%) are credit invisible, with 12.5% lacking a traditional credit score when including those with stale or insufficient credit histories.

Academic research published in MIS Quarterly found that AI-enabled credit scoring enhanced financial inclusion by simultaneously increasing approval rates and reducing default risk—validating alternative-data-based models for underserved populations.

AI-Powered Customer Support and Conversational Assistants

NLP-powered virtual assistants handle high volumes of routine inquiries—account balances, transaction disputes, onboarding questions—with human-like contextual understanding. This reduces call center costs and improves resolution times.

Juniper Research estimated operational cost savings from chatbots in banking reached $7.3 billion globally by 2023, reducing operational costs by approximately 22%. GenAI-powered assistants deliver even greater savings through improved contextual understanding and reduced escalation rates.

24/7 availability differentiates FinTech brands competing on customer experience. AI agents resolve queries in minutes rather than days—reducing churn from support frustration and freeing human agents for complex, high-value interactions.

Automated Regulatory Compliance and Reporting

GenAI monitors real-time transaction streams for AML/KYC compliance triggers, auto-generates regulatory reports, and flags policy violations before they become fines—critical for FinTechs navigating multiple jurisdictions simultaneously.

The compliance burden is substantial:

- Thomson Reuters Regulatory Intelligence tracks approximately 200 international regulatory changes daily, totaling roughly 73,000 alerts annually

- Global financial institutions spend an estimated $270 billion per year on compliance

- Major banks dedicate 7-10% of total revenue to regulatory obligations alone

GenAI automates compliance tracking, reducing manual monitoring workload and compressing report generation from weeks to hours—with audit trails built in.

Algorithmic Trading and Portfolio Intelligence

GenAI synthesizes market sentiment from news, earnings calls, and social data to inform trading strategies and portfolio rebalancing recommendations. WealthTech firms use these outputs to automate research workflows, surface actionable signals faster, and reduce analyst time on data aggregation.

Specific applications gaining traction include:

- Earnings call analysis: NLP models extract forward guidance and sentiment shifts in real time

- Portfolio rebalancing: GenAI recommends adjustments based on drift thresholds and market conditions

- Alternative data integration: Satellite imagery, web traffic, and social signals feed into quant models

- Trade execution optimization: AI identifies optimal entry/exit timing based on multi-source pattern recognition

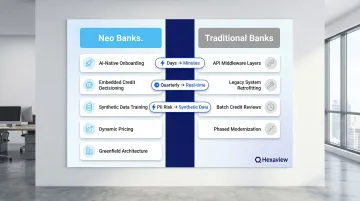

How Neo Banks Are Using GenAI Differently

Neo Banks have no legacy core banking systems, no branch infrastructure costs, and digitally native customer bases. This positions them to deploy GenAI across the full customer lifecycle from day one, building AI directly into product architecture rather than layering it onto outdated systems as an afterthought.

Hyper-Personalized Financial Products at Scale

Neo Banks use GenAI to dynamically tailor product recommendations—savings rates, credit limits, investment bundles—based on individual behavior, life stage signals, and real-time data.

Unlike incumbents retrofitting personalization onto legacy systems through middleware, Neo Banks embed this capability into product architecture. Every interaction becomes a data point; every customer receives a unique financial experience.

AI-Native Onboarding and KYC

GenAI accelerates customer onboarding by automating document extraction, identity verification, and risk profiling—reducing onboarding time from days to minutes. Two deployments show how far this has scaled in practice:

| Neo Bank | Deployment | Scale | Key Outcome |

|---|---|---|---|

| Nubank | AI agents (ReAct paradigm) | 131M customers | Handles debt renegotiation, fraud, credit — audits 100% of conversations via LLM-as-a-Judge |

| Revolut | AI voice agents | 4M+ customers, 30+ languages | 99.7% success rate, 8x faster response, tickets resolved in under 5 minutes |

For traditional banks still running multi-day verification cycles, these benchmarks represent a significant UX gap — one that compounds with every new Neo Bank customer acquired.

Synthetic Data Generation for Model Training

Neo Banks generate synthetic financial datasets mirroring real transaction patterns to train fraud and risk models without exposing customer PII. This addresses GDPR and data residency regulations while enabling model development.

The European Commission launched a Data Hub in October 2024 providing companies with synthetic supervisory data for testing applications and training AI/ML models. The synthetic data replicates statistical properties without including real individuals or identifiable information.

For Neo Banks operating across multiple EU jurisdictions, this means training production-grade models without triggering cross-border data transfer restrictions — removing one of the most persistent blockers to scaling AI in regulated markets.

Dynamic Pricing and Credit Limit Adjustment

GenAI enables Neo Banks to adjust credit limits, interest rates, and product eligibility in near-real-time based on behavioral signals. Bloomberg reported that Nubank's AI features helped boost clients' credit card limits through dynamic risk assessment, shifting credit decisions from quarterly batch reviews to continuous, behavior-driven assessments.

Challenges of Implementing GenAI in Financial Services

Data Quality and Governance

GenAI models are only as reliable as their training data. FinTechs and Neo Banks must invest in data pipelines, lineage tracing, and validation frameworks before deployment. Poorly governed data leads to biased credit decisions and compliance failures.

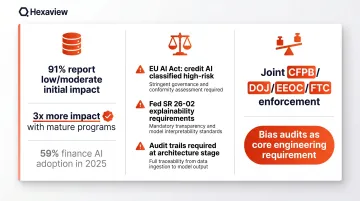

Gartner's November 2025 survey identifies data quality and availability as the single largest obstacle to AI adoption in finance. The numbers tell the story:

- 91% of respondents report only low or moderate impact during initial AI implementation

- Organizations with mature AI programs are nearly 3x more likely to see high impact — the barrier shrinks only with sustained investment

- Finance AI adoption held steady at 59% in 2025 (vs. 37% in 2023), suggesting data and talent gaps are slowing momentum

Regulatory and Compliance Risk

GenAI's probabilistic outputs create tension with financial regulators' demands for explainability and auditability. The Federal Reserve issued revised SR 26-02 model risk guidance in April 2026, updating the original SR 11-7 framework to address AI/ML capabilities.

Under the EU AI Act, Annex III, AI systems evaluating creditworthiness of natural persons are classified as high-risk regardless of sector. High-risk systems face stringent requirements for explainability, bias audits, and compliance timelines.

Firms must embed explainability tooling and audit trails into their GenAI stack at the architecture stage, before any model reaches production.

Algorithmic Bias and Fairness

GenAI models risk perpetuating historical lending or service biases, especially in credit scoring and fraud flagging. The CFPB, DOJ, EEOC, and FTC issued a joint statement on enforcement against discrimination in automated systems, signaling coordinated regulatory attention to algorithmic fairness.

Responsible AI frameworks, bias audits, and diverse training datasets need to be scoped into every consulting engagement — treated as core engineering requirements, given coordinated multi-agency enforcement is now a real operational risk.

Integration with Legacy or Modern Infrastructure

For FinTechs layering GenAI onto existing systems, a full infrastructure overhaul is rarely necessary — or advisable. The right integration approach directly determines how fast capabilities go live and when ROI materializes. Common patterns include:

- API-first architectures that expose GenAI endpoints without disrupting core banking systems

- Middleware layers that translate between legacy data formats and modern AI pipelines

- Phased modernization that delivers quick wins while incrementally retiring technical debt

What to Look for in a GenAI Consulting Partner for FinTech

Financial Domain Expertise is Non-Negotiable

A GenAI partner with deep FinTech domain knowledge—understanding capital markets, wealth management workflows, payment rails, and regulatory environments—delivers faster time-to-value than a generalist AI firm. Domain expertise allows the partner to identify the right use cases, not just deploy models.

Hexaview brings 10+ years of experience in capital markets and wealth management, with recognition on the WealthTech 100 list. This financial domain depth allows Hexaview to translate AI capabilities into business outcomes within regulated environments—a capability generic consulting firms lack.

Security Certifications and Compliance Readiness

In regulated financial environments, the consulting partner must hold verifiable security credentials. SOC 2 Type 2 certification and ISO compliance are baseline requirements for handling sensitive financial data.

Confirm the partner meets your data residency, access control, and audit logging requirements upfront. Hexaview holds SOC 2 Type 2 certification and ISO compliance, ensuring alignment with financial sector security standards.

Production-Proven Delivery, Not Just Prototypes

Partners who demonstrate impressive demos but lack production deployment track records create downstream risk. Look for partners who own the solution through go-live and post-deployment—covering model drift monitoring, retraining pipelines, and integration maintenance.

Ask for case studies with measurable business outcomes, not just architecture diagrams. BCG research from June 2025 found that median AI ROI in finance is only 10%, with one-third of leaders reporting limited or no gains.

Top performers who clear 20%+ returns share three traits:

- Dedicate specific, ring-fenced AI budgets

- Embed AI initiatives into broader transformation programs

- Staff dedicated teams rather than relying on project-by-project resourcing

That execution discipline — not model sophistication — is what Hexaview's delivery model is built around.

Frequently Asked Questions

What is generative AI for fintech?

Generative AI in fintech refers to AI systems that create new outputs—personalized financial advice, synthetic training data, compliance reports, conversational responses—rather than simply analyzing existing data. Applications span fraud detection, credit risk assessment, customer service automation, and regulatory compliance.

How are Neo Banks using generative AI differently from traditional banks?

Neo Banks, unburdened by legacy systems, build GenAI natively into product architecture—enabling AI-driven onboarding, dynamic credit decisioning, and real-time personalization at launch. Traditional banks must retrofit these capabilities onto existing infrastructure through middleware and API layers.

What compliance and security considerations matter most when adopting GenAI in financial services?

Key requirements include explainability for model decisions, GDPR/CCPA data privacy obligations, AML/KYC automation boundaries, and algorithmic bias audits. Any consulting partner operating in regulated financial environments should hold verified certifications such as SOC 2 Type 2 and ISO.

How long does it take to implement a generative AI solution in a FinTech company?

Timelines vary by use case complexity and data readiness. A focused use case like a compliance chatbot may take 8-12 weeks to deploy; an enterprise-wide fraud detection overhaul may require 6+ months. A scoped pilot is usually the fastest route to validated results before full deployment.

What is the ROI of generative AI for FinTech and Neo Banks?

Outcomes include lower fraud losses, reduced customer service costs, and faster loan decisioning. McKinsey finds top performers attribute 10%+ of EBIT to GenAI, while Accenture projects early adopters gain 22-30% productivity improvement and 600 basis points in revenue growth.

How do I choose the right generative AI consulting partner for my FinTech company?

Look for three things: financial domain expertise, a production deployment track record, and verified security/compliance credentials. A partner lacking any of these creates downstream risk in regulated financial environments. Prioritize partners who own solutions through go-live and post-deployment maintenance.