Introduction

FinTech and wealth management firms are under compounding pressure: client expectations keep rising, regulators keep tightening, and manual workflows can't keep up. Compliance costs now consume 19% of annual revenue for financial firms — totaling $61 billion in the US and Canada alone. Meanwhile, 80% of advisor time goes to non-core activities rather than client engagement, creating a productivity gap that threatens growth.

AI agents go well beyond traditional automation. Unlike rule-based tools, they perceive context, make decisions, and execute multi-step workflows with minimal human oversight. The financial services sector is adopting them fast — 70% of banking executives report their firms currently use agentic AI.

This post breaks down:

- How AI agents differ from traditional automation

- The highest-value use cases for FinTech and wealth management

- Essential governance and compliance considerations

- How to build a practical deployment roadmap

Key Takeaways

- AI agents autonomously handle fraud detection, compliance monitoring, portfolio rebalancing, and client communications, freeing human teams for higher-value work

- Wealth management and FinTech firms gain outsized value from AI agents due to data volume, regulatory complexity, and personalization demands

- Security, explainability, and human-in-the-loop controls must be built in from day one for regulated environments

- Start narrow: choose one high-impact, well-documented process, prove ROI, then expand

AI Agents vs. Traditional Automation: What's Actually Different?

Rule-based RPA follows fixed instructions and breaks when conditions change. Generative AI produces content on demand. AI agents go further: they perceive context, make decisions, execute multi-step workflows autonomously, and course-correct as conditions evolve.

Concrete example: A traditional system flags a suspicious transaction. An AI agent investigates it, cross-references watchlists, analyzes transaction patterns across related accounts, and generates a compliance report—all without human intervention.

Three defining capabilities relevant to finance:

- Executes decisions independently within pre-approved parameters

- Learns from new data, market conditions, and regulatory changes in real time

- Coordinates across other agents, APIs, and core systems simultaneously

FinTech and wealth management are particularly well-suited for agentic AI. The combination of massive unstructured data volumes, multi-system workflows spanning CRMs, trading platforms, and compliance tools, and round-the-clock responsiveness requirements is exactly where agent-based architectures outperform point solutions.

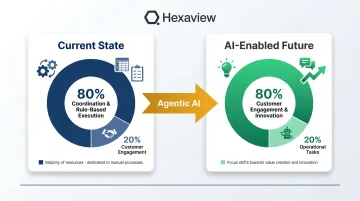

McKinsey research shows that 50–60% of FTEs in banks are tied to operations, and agentic AI can free up 40–70% of capacity within specific processes. McKinsey projects the operational model will flip: from 80% of employee time spent on coordination and rule-based execution to 80% focused on customer engagement, decision-making, and innovation.

Key AI Agent Use Cases for FinTech & Wealth Management

Fraud Detection and Risk Monitoring

AI agents monitor transaction streams in real time using behavioral and pattern analysis, flag anomalies instantly, freeze accounts autonomously within pre-approved parameters, and generate structured incident reports for analyst review.

The scale advantage is significant. Large institutions generate approximately 950 false alerts per million transactions daily, with AML false positive rates at 90-95%. AI/ML can potentially reduce false positives by 50-70%, while processing volumes that would overwhelm human teams.

US consumers reported losing $12.5 billion to fraud in 2024—a 25% increase over 2023. AI agents operating continuously can detect patterns across thousands of accounts that human analysts reviewing cases sequentially would miss.

Regulatory Compliance and KYC/AML

Agents continuously scan transactions and customer data against regulatory requirements, validate KYC documentation, flag discrepancies, and auto-generate audit-ready compliance reports. This reduces both processing time and false positive rates.

30% of institutions require over two months for new client onboarding, with customer abandonment rates during KYC reaching 50-70%. AI can compress that timeline from two months to one week — or days — in wealth management implementations.

Financial crime compliance costs total $206 billion globally, with 79% attributed to personnel. For most firms, automating compliance workflows cuts headcount dependency while shrinking the per-case cost that drives that $206B figure.

Intelligent Credit Underwriting

AI agents gather and normalize applicant financial data from bureau reports, bank statements, and alternative payment histories. They apply credit policy rules, deliver risk scores, approve eligible applications, and surface exception summaries for complex cases.

This reduces days-long manual reviews to minutes. iA Financial Group (5M+ clients, approximately $260 billion in assets) is advancing toward 80% underwriting automation using AI platforms, enabling real-time decisioning and eliminating manual underwriting bottlenecks.

64% of private equity firms report using AI to streamline due diligence processes, demonstrating the broader application of AI-driven document analysis and risk assessment across financial services.

Portfolio Management and Rebalancing

AI agents continuously assess portfolio drift against strategic targets, monitoring ESG mandates, risk-adjusted return thresholds, and sector rotation signals. They either generate rebalancing recommendations or execute pre-approved low-impact trades autonomously — including tax-loss harvesting opportunities that maintain portfolio characteristics while realizing losses within client mandates.

The global robo-advisory market stood at $1.4 trillion in 2024 and is projected to reach $3.2 trillion by 2033 — a trajectory driven by cost pressure on advisors and client demand for always-on portfolio oversight.

Client Communication and Personalized Engagement

Agents handle multi-turn client interactions across channels including chat, email, and voice. They support 24/7 account inquiries and surface proactive, hyper-personalized recommendations based on life events or portfolio performance.

70% of billion-dollar RIAs already use AI for notetaking or call documentation, while 50% plan to implement it for client onboarding. The operational impact compounds quickly at scale: PenFed Credit Union saves 30,000 minutes of labor per day ($3M/year) through automated call summaries, running 700,000+ LLM calls monthly to do it.

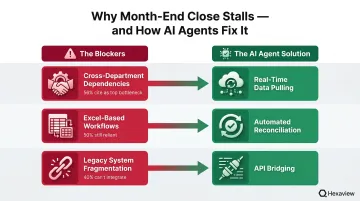

Financial Reporting and Close Acceleration

Agents pull live data from ERP systems, billing tools, and APIs; validate journal entries; reconcile discrepancies in real time; and generate narrative variance reports. This converts periodic manual close cycles into continuous, always-accurate processes.

50% of finance teams take 6 or more business days to close each month; only 18% close in under 3 days. Most teams automate less than 40% of their close process.

The core blockers holding teams back:

- Cross-department dependencies — cited by 56% of teams as their top bottleneck

- Excel-based workflows — still the primary close tool for 50% of finance functions

- Legacy system fragmentation — prevents integration for 40% of organizations

AI agents that operate across systems directly address each of these — pulling data without waiting on department handoffs, replacing manual spreadsheet reconciliation, and bridging legacy systems through API layers.

Where AI Agents Create Outsized Value in Wealth Management

The Advisor Productivity Gap

The average advisor spends up to 80% of their day on non-client-facing work:

- Meeting prep, portfolio reviews, and CRM updates

- Compliance documentation and reporting

- Manual data synthesis across 10+ screens to build a single client picture

AI agents can absorb this operational load—meeting prep, portfolio reviews, CRM updates, compliance documentation—enabling advisors to focus on high-value client strategy. McKinsey estimates that 60-70% of tasks performed by wealth management advisors and support staff can be automated.

Capacity constraints rank as a top-three growth challenge for three consecutive years. The median US advisory firm services 235 households with 6.5 FTEs, and only 24% set formal limits on households per advisor.

Personalization for High-Net-Worth Clients

That productivity gap matters most when it crowds out personalization. AI agents continuously monitor individual portfolios against bespoke mandates — family office constraints, tax situations, legacy holdings, and ESG preferences — and surface actionable insights without manual synthesis. This delivers institutional-grade, real-time guidance at scale, capabilities previously reserved for ultra-HNW clients with dedicated teams.

Democratization for Smaller Firms

Personalization at scale isn't just a competitive advantage for large firms — it's now accessible to RIAs and family offices too. AI agents give smaller wealth management firms the same proactive monitoring and rapid response capabilities as major institutions, without proportional headcount increases.

The structural pressure makes this urgent. The industry faces a projected shortfall of roughly 100,000 advisors by 2034, with 35-40% of advisors expected to retire over the next decade. Firms that don't automate will struggle to maintain service quality as their talent pool shrinks.

Due Diligence Automation for Asset Managers

Agents process hundreds of pages of data room documents, fund fact sheets, and earnings reports—identifying red flags, highlighting discrepancies, and surfacing synergies or risks far faster than human analysts. This compresses weeks of work into hours.

64% of private equity firms report using AI to streamline due diligence, confirming that AI-assisted analysis has moved from experimental to standard practice in complex deal workflows.

Security, Governance & Compliance: What FinTech Firms Must Get Right

Governance Cannot Be Retrofitted

In financial services, autonomous AI systems touching credit decisions, fraud flags, and client portfolios must have auditability, explainability, and human-override mechanisms built into the architecture from the start—not added as an afterthought.

Regulators are actively examining AI use. FINRA Regulatory Notice 24-09 (June 2024) requires firms to review model risk management frameworks for AI, focusing on explainability, bias, data privacy, and third-party AI tools. The SEC is prioritizing enforcement against "AI washing."

Key Components of AI Governance for FinTech

A sound AI governance framework requires:

- Documented AI inventories with risk classifications per use case

- Bias testing and validation protocols

- Model lifecycle monitoring and version control

- Data privacy controls aligned with regulatory requirements

- Structured escalation paths for edge cases

- Human-in-the-loop thresholds for high-stakes decisions

Smaller models purpose-built for compliance use cases often outperform broad public models in regulated environments. Domain-specific training on financial regulations and firm policies delivers more reliable, auditable outcomes.

Data Security Requirements for Agentic Systems

AI agents operate on sensitive client financial data across multiple integrated systems. Firms need end-to-end encryption, role-based access controls, SOC 2-aligned infrastructure, and continuous monitoring to prevent both external breaches and internal misuse.

The average cost of a data breach is $4.88 million overall and $3.28 million in the payment industry. Working with partners who hold relevant security certifications, such as SOC 2 Type 2, reduces vendor risk significantly.

Hexaview holds SOC 2 Type 2 certification and builds Agentforce-powered automation with embedded guardrails — so FinTech and wealth management firms get agentic capabilities without trading away security controls.

The Human-in-the-Loop Imperative

Security controls govern what agents can access — but oversight design governs what they can do. Autonomous agents should operate within pre-approved parameters, with clear escalation thresholds for anything touching significant client impact, regulatory gray areas, or novel edge cases.

The most effective agent workflows build oversight into the architecture: approval gates, confidence thresholds, and exception routing that trigger human review automatically — not because a policy says so, but because the system is built that way.

Building Your AI Agent Roadmap: From Pilot to Production

Selection Framework: Score and Prioritize

Prioritize use cases that are:

- High-impact - Measurable business outcome (cost reduction, time savings, revenue growth)

- Low-risk - Well-documented processes with clear rules

- Currently manual - Human effort that can be reallocated to strategic work

Score candidates on these three dimensions and begin with the top-ranked process rather than attempting wholesale transformation. Fraud detection, compliance document review, and client communication automation consistently rank well on this matrix.

Data Readiness Prerequisites

AI agents amplify the quality of the data they're built on. Fragmented CRMs, siloed trading systems, and inconsistent data definitions will undermine agent performance.

61% of billion-dollar RIAs have initiated or completed a data project as part of strategic planning, yet 35% cite improving data visibility and usage as their top challenge. Firms should assess and address data governance gaps before deployment, not after.

MIT Sloan Management Review identifies poor data quality as a factor that "dooms generative AI projects," noting that feeding bad data to AI models produces untrustworthy results. In short: get your data house in order before writing a single line of agent logic.

Partnership and Infrastructure Decision

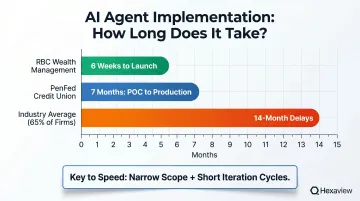

Implementation timelines vary dramatically across institutions:

- RBC Wealth Management launched its Agentforce AI solution in 6 weeks

- PenFed Credit Union moved from POC to production in 7 months

- 65% of institutions experience delays averaging 14 months

Scoping narrowly and iterating in short cycles is the most reliable way to stay closer to six weeks than fourteen months.

Frequently Asked Questions

What are the use cases of AI agents in finance?

Primary categories include fraud detection and risk monitoring, regulatory compliance (KYC/AML), credit underwriting, portfolio management and rebalancing, client engagement automation, and financial reporting acceleration. The highest-value use cases are those where data volumes are high and workflows are currently manual.

Which AI is best for financial services?

There's no single best AI — the right choice depends on the use case. Smaller, domain-specialized models often outperform general models for compliance and credit tasks; larger reasoning models excel at portfolio analysis and reporting. Financial firms should prioritize explainability, auditability, and vendor security certifications.

How are financial services companies securing AI agents?

Firms typically secure AI agents through SOC 2-aligned infrastructure, role-based access controls, end-to-end data encryption, human-in-the-loop oversight for high-stakes decisions, model validation, and documented AI inventories. Regulators expect full auditability and explainability for every AI-driven decision.

What is the difference between AI agents and traditional automation in finance?

Traditional RPA follows fixed rules and breaks when conditions change. AI agents perceive changing data, make contextual decisions, coordinate across systems, and adapt their approach—making them suitable for complex, variable financial workflows that rule-based tools cannot handle.

How long does it take to implement AI agents in a wealth management firm?

A focused pilot on a single well-defined use case — such as compliance document review or client communication — typically runs 3-6 months from scoping to proof of concept. Broader deployment depends heavily on data readiness and legacy system complexity.