Introduction

Wealth management and FinTech firms are sitting on decades of accumulated technical debt. Portfolio management systems, order management platforms, and client reporting tools built in a pre-cloud era now struggle to support real-time analytics, regulatory demands, and client expectations. In financial services, that gap carries fiduciary weight.

Outdated systems create regulatory exposure, data silos, security gaps, and competitive disadvantage. The average bank spends 4.7 times more on compliance for legacy systems than modern alternatives. 62% of organizations still rely on legacy software, consuming 60-80% of IT budgets just maintaining aging infrastructure.

What follows is a practical guide to modernization — what it means for wealth management specifically, which strategies fit different risk profiles, and how to sequence the work without disrupting operations.

Key Takeaways

- Legacy modernization replaces outdated financial systems to improve performance, compliance, and scale

- Aging platforms create regulatory exposure, data silos, and competitive disadvantage

- The 5 R's (Rehost, Replatform, Refactor, Re-architect, Replace) match approach to risk tolerance

- Modernization unlocks real-time data, AI analytics, and better advisor and client experiences

- A phased roadmap reduces disruption while delivering measurable value at each stage

What Is Legacy Software Modernization in Wealth Management and FinTech?

Legacy software modernization is the strategic process of updating, migrating, or replacing outdated systems to align them with current business, regulatory, and technology requirements. It's not always a full replacement—modernization spans a spectrum of interventions ranging from code refactoring to full system rebuilds.

In financial services, "legacy" has a specific look: COBOL-based core banking systems, monolithic portfolio management platforms, manual reconciliation workflows, and CRM databases that can't connect to modern data pipelines. Many wealth management firms still run on systems built in the 1990s or early 2000s—before cloud infrastructure, mobile access, or API-driven architecture existed.

What legacy looks like in practice:

- COBOL still processes an estimated $3 trillion in daily financial transactions, runs 95% of U.S. ATM swipes, and powers 43% of global banking systems

- On-premise portfolio management systems rely on hardcoded business logic, overnight batch processing, and zero API connectivity

- Spreadsheet-based reconciliation handles portfolio valuations, trade settlements, and fee calculations—manually, every time

- Proprietary client reporting tools remain isolated from modern CRM platforms and digital client portals

Legacy Modernization vs. Digital Transformation

Legacy modernization is the prerequisite technical work that makes digital transformation possible. Without it, initiatives like AI-powered portfolio analytics, real-time client dashboards, automated compliance reporting, or open-architecture integrations simply don't work. Modern experiences require modern infrastructure—there's no shortcut around it.

Why Legacy Systems Are a Growing Liability for Financial Firms

Regulatory and Compliance Exposure

Legacy systems were built before current regulatory frameworks like SOC 2, GDPR, MiFID II, and SEC data governance mandates existed. Firms running outdated platforms face mounting compliance gaps.

Companies using legacy systems have a 40% higher likelihood of compliance failures, according to Gartner. In fiscal year 2024 alone, the SEC brought recordkeeping cases resulting in more than $600 million in civil penalties against more than 70 firms. Since December 2021, off-channel communications enforcement has resulted in charges against more than 100 firms and over $2 billion in penalties.

Real compliance failures from legacy systems:

- FINRA fined a broker-dealer and robo-advisory firm $850,000 after coding errors and system transitions caused the firm to fail to retain more than 22 million business-related electronic communications over six years

- The firm was unable to fully respond to 39 regulatory requests from FINRA and the SEC

- More than 500,000 communications went unreviewed by supervisors

Data Silos and Reporting Failures

In wealth management, data accuracy directly underpins portfolio valuations, client reporting, and regulatory filings. Legacy systems create "process debt": business logic hardcoded into workflows, data fragmented across disconnected systems, and no single source of truth.

The result:

- Manual reconciliation consuming hours of advisor and operations time daily

- Error-prone reporting that erodes client trust

- Delayed decision-making due to batch processing overnight instead of real-time data access

- Inability to integrate data from custodians, market data providers, and third-party analytics tools

Security Vulnerabilities That Financial Regulators Won't Ignore

Outdated systems no longer receive security patches, creating exploitable vulnerabilities in environments handling sensitive client financial data. 43% of IT professionals cite security vulnerabilities as their top legacy software concern, according to Saritasa's 2025 survey of 500+ U.S. IT professionals.

In financial services, the stakes are even higher. Verizon's 2025 Data Breach Investigations Report found:

- 3,336 incidents and 927 confirmed data breaches in the Financial and Insurance sector

- System intrusion rose from 36% to 53% of breaches year-over-year

- Vulnerability exploitation as an initial access vector doubled compared to 2024

- The financial sector is the #1 target for denial-of-service attacks

Regulatory implications:

- Organizations running legacy platforms face cyber insurance premium increases of 40-60% or policy non-renewal

- Outdated IT equipment serves as the initial access point in 24% of data breach incidents

- SEC OCIE guidance specifically requires comprehensive patch management, legacy system decommissioning protocols, and reassessing vulnerability profiles when replacing legacy systems

Integration Failures Blocking Modern Capabilities

Modern FinTech ecosystems depend on open banking APIs, real-time market data feeds, robo-advisory tools, and Salesforce-based CRM platforms. Legacy systems cannot connect to these without brittle custom integrations or manual workarounds.

IT teams get locked into maintaining point-to-point integrations that break under load, require constant patching, and block any meaningful innovation. 75% of banks struggle to implement new digital solutions due to legacy infrastructure, according to PYMNTS research.

The Competitive Cost of Inaction

Those integration constraints have a direct competitive cost. FinTech disruptors and digital-native RIAs now offer real-time portfolio views, personalized financial planning tools, and AI-driven insights — capabilities that legacy stacks simply cannot deliver at the same speed.

McKinsey found that between 2013-2023, top-decile U.S. banks achieved 18% total shareholder return per year versus 4% for bottom-decile banks — a 14-percentage-point gap. Tech-enabled strategies can improve return on tangible equity by 3-4 percentage points.

Speed-to-market implications:

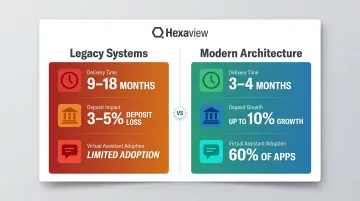

- On modern architectures, solutions are delivered in 3-4 months, compared to 9-18 months for legacy systems

- Digital-only and select regional banks boosted deposits by up to 10% while peers lost 3-5%

- 60% of DIY and 54% of advised wealth management apps now offer virtual assistants, according to J.D. Power's 2025 study of 5,608 investors

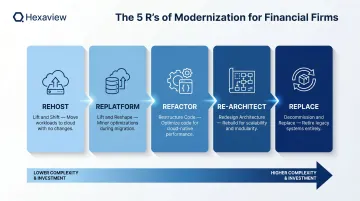

The 5 R's: Choosing the Right Modernization Strategy for Financial Firms

Rehost ("Lift and Shift")

Moving legacy applications to modern infrastructure—typically cloud—with minimal code changes.

When appropriate for financial firms:

- Priority is reducing on-premise infrastructure costs quickly

- Improving availability and disaster recovery without application rework

- Further modernization planned in phases

Limitations: You gain infrastructure benefits but retain underlying architectural debt. Business logic, data models, and integration patterns remain unchanged.

Case study: Discover Financial Services migrated settlement processes from legacy mainframe to AWS, achieving 66% increase in transaction processing speed, pricing change implementation reduced from 6 months to 3 weeks, and expects to save approximately 93% on costs over 5 years.

Replatform ("Lift and Reshape")

Migrating to a new platform while making targeted optimizations—for example, moving a legacy reporting database to a managed cloud database service.

Best fit for: This is a practical first step for wealth management firms with complex, tightly integrated data environments. It reduces operational overhead without requiring a full application rewrite.

Benefits:

- Shifts database management burden to cloud provider

- Enables better scalability and performance

- Maintains existing application code with minimal changes

- Provides foundation for future modernization

Refactor

Restructuring existing code to improve maintainability, performance, and testability without changing its external behavior.

When appropriate: Particularly relevant for firms whose core business logic—portfolio calculation engines, fee billing rules, trade allocation algorithms—is still sound but buried in unmaintainable legacy code.

Why refactor instead of replace:

- Preserves institutional knowledge embedded in code

- Reduces risk of introducing calculation errors

- Maintains regulatory continuity

- Enables incremental improvement while supporting ongoing operations

Re-architect

Redesigning system architecture to adopt modern patterns like microservices, event-driven architecture, or API-first design.

When appropriate: When scalability, real-time processing, or multi-channel client experiences are strategic priorities for FinTech firms.

Case study: Deloitte documented a global wealth management organization that re-architected applications and migrated 20 million lines of legacy code to cloud-based environment, achieving:

- 100% functional equivalence

- 60% reduction in batch processing jobs

- 99.99% system availability

- 25% increase in deployment velocity

- 25% of trading volume now supported by cloud infrastructure

Important note: This requires deeper planning, longer timelines, and a phased delivery approach to manage risk.

Replace

Decommissioning legacy systems entirely and replacing with modern purpose-built platforms or SaaS solutions.

Ideal when: For commodity functions like document management, client onboarding, or basic CRM, replacing with a modern SaaS tool is more efficient than modernizing in place.

Case study: Cevo migrated a 25+ year-old core wealth platform to AWS in 7 months, encompassing 100+ applications, 1,000+ batch processes, and 2,000+ database tables. Results included up to 160% faster batch processing, 2x faster payments performance, and real-time data access.

How to choose: No single strategy fits every system. Map each application against four variables — business criticality, architectural complexity, budget, and risk tolerance — then assign the most appropriate R. Most financial firms end up applying three or four different strategies across their portfolio.

Key Benefits of Modernization for Wealth Management and FinTech Firms

Improved Data Accuracy and Real-Time Analytics

Modernized systems eliminate data silos and enable unified, real-time data pipelines—critical for portfolio valuation, risk monitoring, and regulatory reporting.

Firms leveraging modernized data infrastructure alongside AI and ML capabilities can gain access to:

- Predictive analytics for market risk and portfolio rebalancing

- Anomaly detection for fraud prevention and compliance monitoring

- Personalized investment recommendations based on client behavior and market conditions

Documented outcomes: Technology transformation initiatives in capital markets and wealth management have demonstrated measurable improvements. Hexaview's client engagements in this space have documented a 97% rise in data accuracy and 20,000+ man-hours saved in analysis through modernized data infrastructure.

Enhanced Regulatory Compliance and Security Posture

Modernized systems are built with current compliance frameworks in mind: they embed automated audit trails, role-based access controls, encryption at rest and in transit, and real-time compliance monitoring directly into system architecture.

In practice, this means automated compliance reporting cuts manual effort and error risk, while real-time monitoring flags potential violations before they escalate. Modern systems also receive regular security patches — a basic protection legacy platforms often can't guarantee.

Key compliance capabilities:

- SOC 2 Type 2 certified infrastructure and ISO-aligned development practices

- Automated audit trails with role-based access controls

- Encryption at rest and in transit as a baseline standard

According to PwC research on SOX compliance, a 10% reduction in compliance costs is achievable through automation, according to PwC research on SOX compliance.

Accelerated Advisor Productivity and Client Experience

Legacy platforms that require manual data entry, batch reporting, or multi-system toggling slow advisors down and create inconsistent client experiences.

Financial advisors spend only about 20% of their time in client meetings, according to Kitces Research — the rest goes to meeting prep, research, and administrative tasks that modernization can largely automate.

Modernization impact:

- Integrated CRM platforms with portfolio data reduce system toggling and manual data entry

- Real-time client portals eliminate delays in information access

- Automated workflow engines handle routine tasks like meeting prep and follow-up

- Advisors focus on relationship management and advice delivery instead of administrative burden

Productivity benchmarks: Digital transformation leaders achieve 55% higher productivity and 20-30% reduction in operational costs, according to Docsumo research.

Reduced Total Cost of Ownership and Operational Agility

While modernization requires upfront investment, legacy systems are often more expensive to maintain over time through escalating support costs, specialized talent requirements, and the opportunity cost of delayed feature delivery.

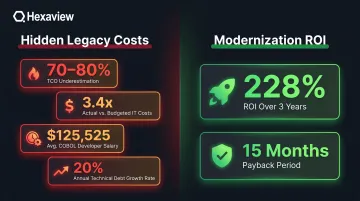

The hidden costs of legacy:

- Financial institutions consistently underestimate the true TCO of legacy systems by 70-80%, according to Deloitte's 2024 Banking Survey

- The average bank discovers actual IT costs are 3.4x higher than initially budgeted when all factors are considered

- Mainframe COBOL developers now earn an average of $125,525 per year, with compensation escalating 25-35% in 2026

- Unaddressed technical debt grows at roughly 20% annually — $1M compounds to $2M in under four years

Modernization ROI: Forrester Total Economic Impact study found 228% ROI from modernizing with Azure PaaS over three years, with an average payback period of 15 months. Infrastructure costs for application development reduced by 40%, and application development speed increased by 50%.

Common Challenges and How to Address Them

Data Migration Complexity and Risk

Migrating decades of client financial data—transaction histories, portfolio records, compliance documentation—is one of the highest-risk elements of any financial services modernization project.

What can go wrong:

- Data loss or corruption during migration

- Business logic embedded in data structures that breaks when moved

- Incomplete mapping of legacy data fields to new system schema

- Compliance gaps during transition periods

FINRA identified data conversion failures in its 2024 Annual Regulatory Oversight Report—where firms failed to maintain controls when converting paper records to electronic records, resulting in records that were not accurate, complete, or readable.

How to address this:

- Thorough data mapping before any migration begins

- Automated validation pipelines to verify data integrity at every stage

- Parallel-run periods where old and new systems operate simultaneously

- Phased migration starting with non-critical data sets

- Treat migration timelines as flexible — rushing this step is one of the most common causes of modernization failures

Organizational Resistance and Change Management

50% of IT professionals cite "the current system still works" as the primary reason for delaying legacy modernization, according to Saritasa's 2025 survey.

That inertia runs especially deep in wealth management. Advisors and operations teams have spent years learning workarounds and memorizing platform quirks — and they fear that a new system will disrupt client service before it improves it.

Addressing that concern early, with transparency and visible quick wins, is what separates successful rollouts from stalled ones.

How to overcome resistance:

- Stakeholder communication that clearly articulates how the new system makes their work easier

- Phased rollouts that minimize disruption and allow teams to adapt incrementally

- Training programs that build confidence before go-live

- Champions within the organization who advocate for modernization

- Quick wins that demonstrate tangible value early in the program

Regulatory Continuity During Transition

Financial firms cannot afford operational downtime or compliance gaps during modernization. Client reporting, trade execution, and compliance workflows must remain uninterrupted throughout the transition.

SEC OCIE guidance makes the stakes clear: firms must reassess vulnerability and risk profiles when replacing legacy systems, and verify that decommissioning hardware or software doesn't introduce new exposures in the process.

Transitional architecture strategies that support this include:

- Running old and new systems in parallel during the cutover period

- Incremental traffic routing that gradually shifts users to the new system

- Rigorous testing before decommissioning legacy components

- Rollback plans if issues emerge post-migration

- Regulatory validation of the new system before legacy decommissioning

Building a Modernization Roadmap for Your Firm

Start with an Outcomes-First Assessment

Before selecting a modernization approach, map your current application portfolio against business impact and technical risk.

Key questions:

- Which systems are mission-critical (core portfolio management, trade execution, compliance reporting)?

- Which handle commodity functions that could be replaced with SaaS solutions?

- Where is legacy debt creating the greatest business constraint?

- What regulatory or security vulnerabilities exist today?

Prioritize based on impact, not age: The oldest system isn't always the most important to modernize first. Focus on where legacy debt is blocking business value or creating unacceptable risk.

Break the Program into Incremental, Deliverable Phases

Large, multi-year "big bang" modernization programs routinely fail because changing business needs outpace the program plan. Only 0.5% of IT projects meet all three measures of success (on time, on budget, and intended benefits), according to McKinsey and University of Oxford research.

Better approach:

- Identify architectural seams that allow you to modernize components independently

- Deliver business value at each phase while decommissioning legacy components progressively

- Validate approach and build internal confidence before tackling higher-risk components

- Allow course correction based on lessons learned in early phases

Example phased approach:

- Phase 1: Migrate non-critical reporting systems to cloud infrastructure (Rehost)

- Phase 2: Modernize data layer and create unified data warehouse (Replatform)

- Phase 3: Refactor core portfolio calculation engine for maintainability

- Phase 4: Re-architect client portal for real-time data access

- Phase 5: Replace legacy CRM with modern Salesforce-integrated solution

Partner with Specialists Who Understand the Financial Services Domain

Executing this roadmap successfully demands more than software engineering skill. Your partner needs genuine fluency in regulatory requirements, portfolio data models, compliance workflows, and the integration patterns unique to financial services.

When evaluating partners, look for:

- SOC 2 Type 2 certification and cloud partnership tiers (AWS, Azure) that signal security maturity

- Demonstrated capital markets and wealth management client history — not just general enterprise experience

- Industry recognition specific to financial technology (for example, WealthTech 100 inclusion)

- Working knowledge of SEC, FINRA, and data governance mandates, not just surface-level awareness

Hexaview Technologies brings over 10 years of specialized experience in capital markets and wealth management modernization, working with firms like LPL Financial and Addepar. Holding SOC 2 Type 2 certification and AWS Select Tier Service Partner status, Hexaview pairs AI Engineering and Data Science depth with the security posture and compliance familiarity financial firms need.

Frequently Asked Questions

What is legacy software modernization?

Legacy software modernization is the process of updating or replacing outdated systems — through approaches ranging from code refactoring to full replacement — to meet current compliance, security, and business requirements. For financial services firms, it's specifically about aligning aging platforms with the speed and integration demands of modern markets.

Is replacing a legacy system worth it?

Yes, though it requires upfront cost and planning. For wealth management and FinTech firms, the cost of inaction typically outweighs modernization: escalating maintenance, growing security exposure, compliance risk, and competitive disadvantage compound over time. An incremental approach reduces risk significantly compared to a full big-bang replacement.

What are the 5 R's of modernization?

The 5 R's cover the full spectrum of modernization options:

- Rehost — lift and shift to cloud infrastructure

- Replatform — migrate with targeted optimizations

- Refactor — restructure code for maintainability

- Re-architect — redesign for modern distributed patterns

- Replace — swap legacy systems for modern platforms

Each represents a different level of investment. Most firms apply a combination rather than committing to a single approach.

What are examples of legacy software modernization?

Common financial services examples include:

- Migrating an on-premise portfolio management system to cloud-based architecture

- Refactoring a monolithic trade reconciliation platform into microservices

- Replacing a legacy CRM with a Salesforce-integrated solution connected to portfolio data and client portals

What are common examples of legacy software?

In financial services: COBOL-based core banking systems, on-premise portfolio management platforms from the 1990s-2000s, mainframe-based order management systems, and proprietary client reporting tools that lack API connectivity. Many wealth management firms still run systems built before cloud infrastructure, mobile access, or API-based integration became standard.

What is the difference between cloud-native applications and legacy systems?

Legacy systems were built for on-premise, monolithic architectures and struggle to scale or integrate with modern tools. Cloud-native applications are designed from the ground up for distributed, API-driven environments — enabling elasticity, continuous deployment, and native integration with modern data and AI services.