Introduction

Neo banks and fintechs operate under conditions traditional banks never faced: scale fast, serve customers 24/7, and stay compliant—all with leaner teams. Manual KYC reviews stretching 31-60 days, fraud losses climbing 25% year-over-year, and compliance budgets eating up to 40% of operating expenses aren't just frustrating. They're growth killers.

The answer isn't hiring more analysts. It's deploying AI employees that handle 80% of routine workflows autonomously—from document ingestion to fraud response—without missing a compliance update or clocking out.

This article covers what agentic AI actually is, why it goes further than conventional automation or generative AI, the highest-value use cases for fintechs and neo banks, and how NemoClaw-powered AI employees make it operational today.

Key Takeaways

- Agentic AI autonomously plans, decides, and executes multi-step workflows — KYC, fraud detection, loan origination — without waiting for human prompting at each step

- Neo banks deploy AI faster than legacy banks, leveraging cloud-native architecture with no decades-old tech debt slowing integration

- Real-world impact: up to 40% cost reduction, 60% faster processing, and 3–15% revenue gains per relationship manager

- Governance is non-negotiable: compliance-by-design, human oversight, explainability, and SOC 2 certification are baseline requirements for regulated institutions

- NemoClaw provides AI employees built specifically for fintech workflows, with audit trails and escalation pathways included from day one

What Is Agentic AI — And Why Traditional Automation Falls Short

The Three Core Capabilities That Define Agentic AI

Agentic AI is technology that moves beyond reactive content generation to independent action. McKinsey defines it as systems that handle tasks that are "less structured, more personalized, and that effectively happen only once"—decisions and workflows that traditional automation cannot touch.

Three capabilities distinguish agentic AI:

- Autonomy — Independent decision-making without constant human prompting or supervision

- Adaptability — Real-time learning from feedback, new data, and changing conditions

- Coordination — Multi-agent communication across APIs, databases, and financial systems to complete end-to-end workflows

Traditional rule-based automation (RPA) follows fixed if-then logic. It automates narrow, repetitive tasks but suffers from the "fingers and toes problem"—handling only fragments of a workflow. Generative AI creates content on demand but cannot take action or execute multi-step plans. Agentic AI closes the gap: it generates answers and completes the task.

Multi-Agent Orchestration: How AI Employees Collaborate

Agentic systems use an orchestrator agent that assigns tasks to specialized utility agents—data extraction, compliance checks, reporting—which work in sequence or parallel toward a shared goal. The result is a coordinated team architecture, not a single-purpose tool.

Each agent functions as an AI employee trained for a specific role, equipped with long-term memory, and designed to achieve outcomes. A KYC AI Employee, for example, handles the full case lifecycle:

- Ingests and parses identity documents

- Validates data against authoritative sources

- Flags anomalies and suspicious patterns

- Cross-references global watchlists

- Closes the case with a documented audit trail

Gartner predicts that 15% of day-to-day work decisions will be made autonomously through agentic AI by 2028, up from 0% in 2024. However, 40% of agentic AI projects will be canceled by end of 2027 due to high costs, unclear value, or lack of risk controls—underscoring the importance of purpose-built platforms over custom builds.

Real-World Productivity Gains

McKinsey reports that banks deploying agentic AI in a single frontline domain see measurable gains:

- 3–15% higher revenues per relationship manager

- 20–40% lower cost to serve within targeted domains

Yet the same McKinsey research finds nearly 80% of institutions report no significant bottom-line impact. The gap isn't capability—it's implementation. Institutions that see results rewire complete workflows end to end, rather than layering AI onto isolated tasks.

Why FinTechs and Neo Banks Are Uniquely Positioned to Win

The Legacy-Tech Disadvantage of Incumbent Banks

Traditional banks face a structural handicap: decades-old core systems built on mainframes, batch processes, and fragmented data silos. Integrating agentic AI into these environments requires costly, time-consuming middleware layers and legacy system modernization. Neo banks and fintechs, built on cloud-native architecture at launch, deploy AI employees into existing stacks in weeks, not quarters.

The Business Case for Lean Teams

A comparative study found that neo banks generate approximately €119,430 in average profit per employee (versus €42,852 at traditional banks in Europe — a nearly 3x gap). AI-driven productivity gains compound even more dramatically at this efficiency baseline.

A fintech with 50 employees can use agentic AI to cover functions that would otherwise require 150+ staff, including:

- Compliance monitoring and regulatory reporting

- Fraud detection and transaction screening

- Customer onboarding and KYC verification

- 24/7 support and account management

That capacity advantage scales fast. The US neobank customer base grew from 86 million to nearly 150 million accounts in 30 months — precisely because cloud-native infrastructure absorbs growth without proportional headcount increases.

AI Employees in Action: Key Use Cases for FinTechs and Neo Banks

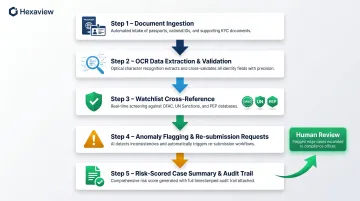

KYC and AML Compliance

Manual KYC reviews are a massive cost center. Fenergo reports that KYC represents 31-40% of total compliance budgets at nearly one-third of banks. A single corporate client review costs $1,501–$3,500 and takes 31–60 days for 40% of banks. One-third of banks employ 1,001–1,500 full-time employees for KYC alone.

An AI employee autonomously:

- Ingests identity documents (passports, utility bills, corporate registrations)

- Extracts and validates data points using OCR and structured field mapping

- Cross-references watchlists (OFAC, UN, PEP databases) in real time

- Flags missing or inconsistent information for re-submission

- Generates case summaries with risk scores for human compliance review

Result: processing time drops from weeks to hours. Manual review shifts from data entry to judgment calls on flagged edge cases.

Fraud Detection and Response

Fraud losses are accelerating. The FTC reports US consumers lost $12.5 billion to fraud in 2024, a 25% year-over-year increase. Globally, card fraud reached $33.41 billion.

Rule-based systems operate on fixed thresholds: flag any transaction over $10,000. That approach cannot adapt to novel fraud schemes or behavioral anomalies. An AI fraud agent:

- Monitors real-time transaction patterns and user behavior continuously

- Identifies novel fraud patterns as they emerge, not just known signatures

- Reduces false positives by learning legitimate customer behavior over time

- Autonomously triggers pre-approved responses: account freeze, step-up authentication, transaction hold

- Escalates ambiguous cases to human analysts with full context and risk assessment

Fraud is contained before it escalates — often before a human analyst sees the alert.

Loan Origination and Credit Decisioning

AI credit scoring models improve default prediction accuracy by 15-25%, allowing institutions to approve more applicants while maintaining or reducing portfolio risk. Lenders using AI-based scoring have reduced per-loan origination costs by up to 14%, cut defect rates by 40%, and achieved a 5-day shorter loan cycle.

An AI underwriting employee handles the end-to-end workflow:

- Collects and verifies borrower data (income, employment, credit history)

- Runs credit bureau checks and validates data consistency

- Flags compliance issues (fair lending, affordability requirements)

- Routes edge cases—non-standard income sources, thin credit files—to human underwriters

- Approves routine applications autonomously with full audit trail

Human underwriters focus on high-judgment cases requiring nuanced risk assessment, not data gathering.

Regulatory Note: AI systems used to evaluate creditworthiness are classified as high-risk under the EU AI Act. Fines for non-compliance reach up to €15 million or 3% of global turnover. Explainability and human oversight are non-negotiable.

Proactive Personalized Customer Engagement

Most chatbots sit idle until a customer asks a question. A proactive AI employee works differently: it monitors spending patterns, anticipates issues, and initiates solutions before the customer notices a problem.

Example workflow: The AI detects a customer approaching an overdraft based on recurring bills and current balance. It autonomously:

- Initiates a temporary credit line increase (pre-approved policy)

- Sends a personalized savings nudge with actionable recommendations

- Recommends a product upgrade (premium account with overdraft protection)

McKinsey research on AI-driven engagement puts the stakes in stark terms:

- 65% increase in cross-sales at banks using proactive AI engagement

- 30% net annual growth in primary customers

- 57% of customers would switch to a third-party gen AI financial agent if their bank doesn't offer one

That last figure matters most. Inaction doesn't just limit growth — it risks ceding the customer relationship entirely.

NemoClaw: Pre-Built AI Employees for FinTech Workflows

NemoClaw delivers AI employees built specifically for KYC, fraud detection, loan origination, and customer engagement. Compliance guardrails, escalation pathways, and audit trails come integrated from day one — not bolted on after deployment. Built on Hexaview's SOC 2 Type 2 certified infrastructure, NemoClaw gives FinTech teams a foundation they can configure and go live with, rather than engineer from scratch.

Risks, Governance, and Built-In Compliance for Regulated Institutions

Algorithmic Bias and Unfair Decisions

AI agents trained on historical financial data can perpetuate biases in credit, lending, or onboarding. Firms must use explainable AI (XAI) models that provide auditable reasoning behind every decision—not just an output.

The Apple Card case resulted in $89 million in penalties (Apple fined $25 million, Goldman Sachs $45 million) for algorithmic credit system failures. "The algorithm decided" is not a legally defensible explanation under CFPB Circular 2023-03.

Expanded Cybersecurity Attack Surface

Agentic systems that communicate across APIs and external tools create new attack vectors. McKinsey reports that 80% of organizations experienced AI-related security incidents, and fewer than 25% have established guardrails for generative AI.

Essential controls include:

- Role-based access controls (RBAC) limiting agent permissions to necessary systems only

- Least-privilege permissions preventing lateral movement across infrastructure

- Continuous monitoring dashboards detecting anomalous agent behavior in real time

- Adversarial attack testing validating resilience against prompt injection and data exfiltration

Human-in-the-Loop as a Compliance Pillar

AI employees handle routine, low-risk tasks autonomously but escalate high-stakes or anomalous decisions to human reviewers. This "compliance by design" architecture is precisely what makes agentic AI deployable in regulated environments.

That requirement isn't arbitrary — EU AI Act, Article 14 mandates human oversight for high-risk AI systems, explicitly covering underwriting and credit decisions. Non-compliance carries penalties up to €15 million or 3% of global turnover, whichever is higher.

Data Governance and Model Drift

Data quality management, feedback loops, and real-time validation protocols are recurring operational costs, not one-time setup tasks. Firms that treat governance as a permanent function build the audit trails and model stability that regulators expect to see.

Critical gap: The Federal Reserve's revised SR 26-2 guidance (April 2026) explicitly excludes generative AI and agentic AI models from its scope. FinTechs must develop internal model governance standards for agentic systems until dedicated regulatory frameworks are established.

How NemoClaw Powers AI Employees for FinTech and Neo Banks

Pre-Built, Role-Specific AI Employees

NemoClaw is Hexaview's agentic AI platform delivering AI employees designed for FinTech and neo bank workflows:

- KYC & AML Compliance — Document ingestion, data extraction, watchlist cross-referencing, case summaries

- Fraud Detection — Real-time transaction monitoring, behavioral analysis, autonomous response triggers

- Loan Origination — Data collection, credit bureau checks, compliance validation, underwriter escalation

- Customer Engagement — Proactive monitoring, personalized recommendations, autonomous issue resolution

The platform is SOC 2 Type 2 certified and built with financial-grade security as a foundational requirement.

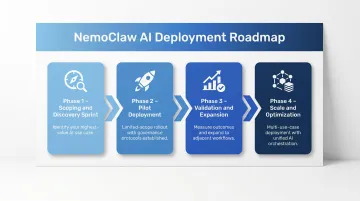

Phased Deployment Without Rip-and-Replace

NemoClaw integrates with existing FinTech stacks via APIs—no infrastructure overhaul required. Deployment follows a phased approach:

- Scoping and discovery sprint — Identify highest-value, low-risk use case (typically KYC document processing or fraud alerting)

- Pilot deployment — Launch with limited scope, establish governance protocols and escalation pathways

- Validation and expansion — Measure outcomes (processing time, cost reduction, accuracy), expand to adjacent workflows

- Scale and optimization — Deploy across multiple use cases with unified orchestration layer

Each phase includes built-in escalation pathways and audit logs as standard components. Every agent action is traceable for regulatory review — no custom additions required.

Credibility Anchored in FinTech Domain Expertise

Hexaview brings 10+ years of capital markets and wealth management expertise, recognition on the WealthTech 100 list, and a client roster including LPL Financial and Addepar. NemoClaw is built by practitioners who understand FinTech workflows from the inside, which shapes every design decision in the platform.

That experience shows up in the platform's track record:

- Automated complex compliance workflows for institutional clients

- Modernized legacy trade and order management platforms

- Delivered advisor billing automation at institutional scale

Frequently Asked Questions

What is agentic AI in finance?

Agentic AI refers to autonomous systems that plan, execute, and adapt multi-step financial workflows — such as KYC, fraud detection, and credit decisioning — with minimal human intervention. Unlike static automation or GenAI chatbots, it combines real-time decision-making, learning, and cross-system coordination to complete tasks end-to-end.

How is AI used in the fintech industry?

AI powers fraud detection, loan origination, KYC/AML compliance, personalized customer engagement, and regulatory reporting. Agentic AI goes further, enabling end-to-end autonomous execution rather than just decision support or content generation.

What are agentic AI technologies?

Agentic AI systems combine large language models (LLMs), retrieval-augmented generation (RAG), reinforcement learning, and multi-agent orchestration frameworks. Specialized agents collaborate, access external tools, and execute complex workflows autonomously — with human oversight reserved for high-stakes decisions.

How is agentic AI different from generative AI?

Generative AI creates content in response to a prompt but stops there. Agentic AI autonomously plans and executes multi-step tasks, interacts with external systems (APIs, databases), and adapts based on real-time outcomes — moving from producing an answer to actually completing the work.

Is agentic AI safe for regulated financial institutions?

Yes, when deployed with proper governance: explainable AI, human-in-the-loop controls, role-based access, compliance-by-design principles, and continuous monitoring. SOC 2 Type 2 certification is a meaningful signal that a platform is ready for regulated production environments.

How can a neo bank get started with AI employees?

Begin with a clearly scoped, low-risk use case — KYC document processing or fraud alerting are practical starting points. Establish governance and escalation protocols before deployment, not after. Hexaview's NemoClaw platform provides pre-built AI employees purpose-built for FinTech, with compliance controls and audit trails included from day one.