Introduction

Wealth managers and asset managers are drowning in data but starving for foresight. Every day, terabytes of market signals, client interaction logs, and portfolio metrics flow through custody systems, CRMs, and trading platforms.

Yet most firms still make million-dollar allocation decisions using backward-looking quarterly reports. By the time spreadsheets are reconciled and decks circulated, market conditions have shifted — and client dissatisfaction has already taken root.

Predictive analytics and AI are changing this dynamic, shifting wealth management from reactive reporting to forward-looking decision-making. 77% of wealth management firms now report improved decision-making with AI-driven predictive analytics, yet only 20% have deployed AI for client-facing tasks — a gap that represents both the challenge and the opportunity.

This article covers:

- What predictive analytics specifically means for wealth and asset management

- The highest-ROI use cases driving adoption today

- Measurable business outcomes from production deployments

- What a production-ready AI development process looks like when regulatory compliance and data complexity are non-negotiable

Key Takeaways

- Predictive analytics in wealth management forecasts portfolio performance, client behavior, and risk exposure using ML models trained on historical trade data, CRM signals, and market indicators

- Top use cases: portfolio drift prediction and rebalancing optimization, client churn detection, alternative data analysis for alpha generation, compliance and risk scoring, and advisor productivity tools

- Firms deploying AI-powered predictive analytics achieve up to 25% faster decision cycles, 35% better risk management outcomes, and measurable improvements in client retention and AUM protection

- Production-ready systems require domain-specific data pipelines, regulatory-aware model architectures with built-in explainability, and MLOps infrastructure for drift monitoring and retraining

- Choosing an AI partner with 10+ years in capital markets and wealth management ensures systems meet regulatory standards and reach production reliably

What Is Predictive Analytics in Asset and Wealth Management?

Predictive analytics in wealth and asset management refers to the use of statistical algorithms, machine learning models, and historical financial data to forecast future outcomes before they occur. Unlike dashboards and reporting tools that describe what already happened last quarter, predictive systems analyze patterns in market data, client transactions, CRM activity logs, and macroeconomic indicators to generate probability-scored forecasts — such as which portfolios will drift beyond target allocation thresholds, which high-net-worth clients are at elevated churn risk, or which asset positions face elevated drawdown exposure in the next 30 to 90 days.

The data landscape in wealth management creates both unique opportunities and complex engineering challenges. Firms work with:

- Structured data: Trade history, AUM figures, portfolio holdings, custodian feeds, performance metrics

- Semi-structured data: CRM activity logs, advisor notes, client communication records, compliance documentation

- Alternative data: News sentiment scores, earnings call transcripts, satellite imagery, web traffic signals, macroeconomic feeds

This volume, variety, and sensitivity of data means generic predictive analytics frameworks built for e-commerce or SaaS applications fail when applied to wealth management. Regulatory requirements for model explainability, data lineage documentation, and auditability demand architectures designed specifically for these constraints.

The global AI in asset management market was valued at $2.61 billion in 2022 and is projected to reach $17.01 billion by 2030, a compound annual growth rate of 24.5%. Firms that delay adoption aren't just missing an efficiency opportunity — they're falling behind competitors making faster, more accurate decisions with the same data.

Predictive AI vs. Generative AI: What Wealth Managers Need to Know

The distinction between predictive AI and generative AI is critical when evaluating technology vendors and setting project expectations.

Predictive AI uses historical data to produce probability-scored forecasts. A model trained on two years of CRM engagement, transaction frequency, and portfolio activity might output: "This client has a 74% likelihood of reducing AUM by more than 20% in the next 90 days." It identifies patterns in existing data and projects them forward — no content generation involved.

Generative AI creates new content based on learned patterns. ChatGPT generates text by predicting the next most likely word in a sequence. It doesn't forecast future events from structured financial data; it produces original outputs that simulate human-written content. Powerful for communication tasks — not for portfolio risk forecasting.

As IBM's Chief AI Engineer Nicholas Renotte explains: "Lots of businesses want to generate a financial forecast, but that's not typically going to require a gen AI solution, especially when there are models that can do that for a fraction of the cost."

For wealth management systems, the distinction has direct build implications. A client churn prediction engine requires a predictive ML model with feature engineering on CRM and portfolio data — trained to recognize patterns that precede attrition. Deploying a large language model for this use case wastes budget and delivers the wrong output entirely.

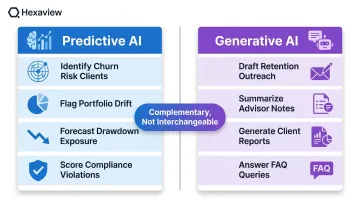

The two categories are complementary, not interchangeable:

| Use Case | Right Tool |

|---|---|

| Identify clients at churn risk | Predictive ML model |

| Flag portfolios approaching drift thresholds | Predictive ML model |

| Draft personalized retention outreach | Generative AI (LLM) |

| Summarize advisor meeting notes | Generative AI (LLM) |

Predictive AI surfaces the signal. Generative AI helps communicate it. Conflating the two at the architecture stage is one of the most expensive mistakes wealth tech teams make.

Key Use Cases of Predictive Analytics in Wealth and Asset Management

Portfolio Optimization and Rebalancing

Traditional portfolio rebalancing triggers on fixed thresholds — when an asset class drifts 5% from its target allocation, the system flags it for review. This rules-based approach ignores forward-looking signals: changing correlations between asset classes, shifts in volatility regimes, tax-loss harvesting opportunities, and transaction cost optimization.

Machine learning models analyze portfolio holdings, historical return distributions, risk factor exposures, and correlation structures to predict drift trajectories and recommend rebalancing actions proactively. Instead of reacting to drift after it crosses a threshold, the model forecasts when drift will occur and suggests optimal timing to minimize transaction costs and tax impact.

Research published in Frontiers in Artificial Intelligence identifies key ML approaches for portfolio management, including Hierarchical Risk Parity (HRP) for improving robustness of risk allocation schemes and Deep Reinforcement Learning (DRL) for capturing dependencies between risk aversion, portfolio characteristics, and dynamic allocations. The review notes: "The core objective of rebalancing is to manage risk concerning the target asset allocation, prioritizing risk management over solely maximizing returns."

Alternative data integration amplifies this capability. A long-short portfolio strategy based on information acquisition activity — specifically SEC EDGAR search traffic as a proxy for institutional interest — generated a monthly abnormal return of 80 basis points that was not reversed in the long run, according to research cited in the same review.

Client Risk Profiling and Churn Prediction

Predictive models built on CRM activity, transaction frequency, life event signals, and advisor interaction logs can identify which clients are at elevated risk of reducing assets under management or churning entirely — typically 30 to 90 days before they act.

The business case is direct: acquiring a new customer costs approximately 5 times more than retaining an existing one. Yet in wealth management, 20% of clients leave their advisor within the first year and 25% leave after year two.

That attrition is largely preventable. An industry-wide average retention rate of 97% among established relationships shows that firms catching early warning signs can keep clients they would otherwise lose.

A predictive churn model flags at-risk relationships before the client makes a final decision by monitoring signals such as:

- Declining login frequency or platform engagement

- Reduced response rates to advisor outreach

- Missed review meetings without rescheduling

- Portfolio withdrawals without a corresponding life event

- Decreased use of planning or goal-tracking tools

Early intervention — proactive portfolio review, fee structure adjustment, or service model changes — becomes possible when the signal arrives weeks in advance, not after the account transfer request is filed.

Market Forecasting and Alternative Data Analysis

Asset managers are increasingly ingesting alternative data sources to generate alpha signals ahead of consensus. 78% of funds now use or expect to use alternative data, up from 52% in 2016. The global alternative data market was valued at $11.65 billion in 2024, with provider revenues projected to grow 29-fold by 2030 at a compound annual growth rate of 53%.

Alternative data includes:

- Sentiment analysis from earnings call transcripts, SEC filings, and news coverage

- Geospatial signals from satellite imagery tracking retail foot traffic, shipping activity, or construction progress

- Web behavior data such as job posting volumes, product search trends, or app download rankings

- Macroeconomic feeds including credit card transaction volumes, employment indicators, or supply chain disruption signals

Predictive models ingest these signals alongside traditional financial statements and price history to forecast asset price movements, sector rotation opportunities, and drawdown risk. A survey of 100 hedge fund managers managing approximately $720 billion in AUM found that 53% are current users of alternative data, with market leaders targeting at least a 10x return relative to the all-in cost of any new alternative data sets. 72% of users say alternative data is important or very important to their value proposition.

This use case requires production-grade data pipelines capable of ingesting unstructured text, time-stamped event feeds, and high-frequency streaming data — along with model validation processes that ensure signals are statistically significant and not artifacts of overfitting.

Risk Management and Regulatory Compliance Scoring

The same data infrastructure that powers alpha generation also supports a firm's control environment. Predictive models applied to transaction data, client profiles, and portfolio exposures can flag concentration risk, liquidity shortfalls, and compliance exceptions before they become audit findings or enforcement actions.

Use cases include:

- Concentration risk detection: Identifying portfolios approaching single-issuer or sector concentration limits before breaches occur

- Liquidity risk forecasting: Predicting cash flow needs and margin call exposure under stress scenarios

- Suitability violation screening: Flagging clients whose portfolios deviate from documented risk tolerance and investment policy statements

- AML and fraud detection: Scoring transactions for patterns consistent with money laundering, account takeover, or synthetic identity fraud

The regulatory context makes explainability non-negotiable. SEC, FINRA, and fiduciary duty requirements mean model outputs must be auditable and interpretable — not black boxes. FINRA explicitly recommends that firms using AI-based applications review and update their model risk management frameworks to address the unique challenges that AI presents, and consider whether existing supervisory systems and procedures are adequate under Rule 3110.

Up to 35% improvement in proactive risk management outcomes is achievable using AI compared to traditional methods, according to PwC Strategy& analysis. This gain comes from shifting from reactive reporting — identifying risk after it has materialized — to receiving probability-scored warnings 30 to 60 days in advance.

Advisor Productivity and Lead Scoring

Wealth management firms with large advisor networks use predictive analytics to prioritize which prospects are most likely to convert, which existing clients are ready for a next-best-action conversation, and which accounts are under-served relative to their potential.

Lead scoring models analyze:

- Engagement signals: Email open rates, content downloads, webinar attendance, website visit frequency

- Demographic and firmographic data: Age, investable assets, employment status, proximity to retirement

- Behavioral patterns: Response time to outreach, question complexity, scheduling consistency

AI-driven task-based efficiency has the potential to achieve 20% to 30% time savings for advisors, according to McKinsey. Morgan Stanley's CEO has stated that AI could save financial advisors 10 to 15 hours per week — time previously spent on data entry, report generation, compliance documentation, and administrative follow-up.

Advisor productivity tools surface next-best-action recommendations at the moment they matter — "Client X is approaching required minimum distribution age and has not scheduled a tax planning review" or "Prospect Y has downloaded three retirement planning guides in the past two weeks and has a 78% conversion probability." That specificity shifts advisor time from pipeline maintenance to client outcomes.

Business Benefits of AI-Powered Predictive Analytics for Wealth Managers

Faster, More Confident Decision-Making

Predictive analytics compresses the cycle between data observation and actionable insight. Instead of quarterly portfolio reviews that analyze what happened three months ago, advisors and portfolio managers receive real-time alerts when risk exposures cross model-defined thresholds or when client engagement patterns signal attrition risk.

Up to 25% improvement in decision-making speed and accuracy is achievable through modular data pipelines and context management in financial services, according to PwC analysis. 77% of wealth management firms report improved decision-making with AI-driven predictive analytics.

Improved Data Accuracy and Analytical Depth

Manual data reconciliation across custodian feeds, portfolio management systems, and CRM platforms consumes thousands of analyst and advisor hours annually.

Errors in data mapping, missing transactions, and schema mismatches compound over time, degrading the reliability of performance reporting and compliance documentation.

Hexaview has achieved a 97% rise in data accuracy and saved over 20,000 man hours in analysis for wealth management clients by automating data pipeline construction, schema normalization, and quality validation checks. This shifts advisor and analyst time from data reconciliation to client-facing strategic work — portfolio planning, tax optimization, estate planning, and relationship management.

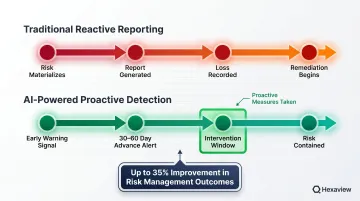

Proactive Risk Management Instead of Reactive Reporting

Traditional risk reporting identifies problems after they've materialized: a portfolio that breached concentration limits last quarter, a client who reduced AUM last month, a compliance gap discovered during an annual audit.

Predictive analytics shifts this timeline forward by 30 to 60 days. Two of the most impactful applications:

- Portfolio risk detection: A model trained on historical drawdown events flags elevated exposure to correlated risk factors before market stress occurs

- Client retention signals: A churn prediction model surfaces at-risk clients early enough to intervene with service adjustments or a timely advisor call

Up to 35% improvement in proactive risk management using AI compared to traditional methods represents the difference between containing a risk event and reporting it as a realized loss.

Revenue Protection Through Client Retention

A predictive churn model that identifies five at-risk high-net-worth clients per quarter and enables successful intervention at a firm managing $2 billion in AUM has direct, quantifiable revenue impact.

Here's what that looks like in practice:

- Average HNW client AUM: $2,000,000

- Annual advisory fee: 1% = $20,000 per client

- Clients identified and retained per quarter: 5

- Annual revenue protected: $100,000

Over a multi-year relationship, retained clients also generate referrals and additional asset inflows — meaning the $100,000 in protected annual fees is a floor, not a ceiling, on the system's return.

How Predictive Analytics Solutions Are Built for Financial Services

Data Pipeline Design and Integration

The first engineering challenge is constructing pipelines that ingest data from custodians (Fidelity, Schwab, Pershing), portfolio management systems (Advent, Addepar, Orion), CRM platforms (Salesforce, Redtail, Wealthbox), market data feeds (Bloomberg, Refinitiv, FactSet), and alternative data sources — then normalize it into a unified schema suitable for model training.

Data arrives in different formats: FIX protocol messages, SFTP file drops, REST APIs, batch CSV exports, and real-time streaming feeds. Schema inconsistencies are common: one custodian reports realized gains in one field structure, another combines realized and unrealized in a summary record, and a third requires calculation from transaction-level data.

Data quality remediation is typically the longest phase in a wealth management AI project. Common issues include:

- Missing or null transaction timestamps

- Inconsistent security identifiers (CUSIP vs. ISIN vs. ticker symbol)

- Duplicate records from multiple data sources

- Currency conversion errors in multi-currency portfolios

- Corporate action adjustments not reflected in historical price series

Production pipelines require automated validation checks, data lineage tracking, and exception handling workflows that flag anomalies for human review before they propagate into model training datasets.

Model Selection and Feature Engineering for Financial Data

Tree-based gradient boosting models such as XGBoost and LightGBM remain the dominant choice for tabular financial data in regulated environments. A widely cited NeurIPS 2022 paper with over 3,000 citations benchmarked tree-based models against deep learning on 45 tabular datasets and found tree-based models consistently superior for medium-sized datasets (under approximately 10,000 samples).

Why do gradient boosting models dominate in wealth management predictive analytics?

- Interpretability: Tree-based models can be decomposed into decision rules that compliance teams and auditors can review

- Robustness on structured data: They handle missing values, mixed data types, and non-linear relationships without extensive preprocessing

- Regulatory explainability: SHAP (SHapley Additive exPlanations) and LIME (Local Interpretable Model-agnostic Explanations) values can be generated to explain individual predictions

Time-series models such as ARIMA and LSTM neural networks are used for market forecasting use cases where sequential dependencies and temporal patterns are critical — such as predicting volatility regimes, interest rate movements, or sector rotation timing.

Feature engineering in wealth management contexts requires domain expertise. Effective features include:

- Client engagement velocity: Change in CRM activity over trailing 30, 60, 90 day windows

- Portfolio concentration metrics: Herfindahl index, top-10 position weights, sector exposure ratios

- Risk factor betas: Sensitivity to equity, interest rate, credit spread, and commodity factors

- Transaction pattern anomalies: Withdrawals during periods inconsistent with historical behavior

- Advisor interaction frequency: Meetings per quarter, response time to client requests, proactive outreach volume

Regulatory-Aware Model Architecture

In wealth management, model outputs must be explainable to regulators and compliance teams, not merely accurate. This requirement drives specific architectural decisions:

- SHAP and LIME explainability: Every prediction must be decomposable into feature-level contributions so compliance can answer "Why did the model flag this client as high churn risk?"

- Model cards and documentation: Production systems maintain version-controlled documentation describing training data sources, feature definitions, performance metrics, and validation test results

- Data lineage tracking: Every prediction must be traceable back to source system records for audit purposes

- Drift detection and monitoring: Automated systems flag when input data distributions shift or model performance degrades, triggering human review

FINRA explicitly states that firms employing AI-based applications should review and update their model risk management frameworks to address the unique challenges AI presents. A model that produces accurate predictions but fails regulatory interpretability requirements won't pass compliance validation.

Hexaview's SOC 2 Type 2 certification and 10+ years of experience in capital markets and wealth management mean these requirements are built into every engagement from the outset, before a single model reaches a compliance desk.

Production Deployment and MLOps

A model delivered as a Jupyter notebook or a batch script is not production-ready. Production deployment in a wealth management context requires:

- Low-latency prediction APIs: Real-time scoring integrated with portfolio management systems and CRM platforms

- Automated drift monitoring: Systems that detect when market regime changes, client behavior shifts, or data quality issues invalidate model assumptions

- Retraining pipelines: Scheduled workflows that retrain models as new data accumulates, validate performance on holdout datasets, and deploy updated versions without service interruption

- Rollback and version control: Ability to revert to previous model versions if production performance degrades

- Monitoring dashboards: Real-time visibility into prediction latency, feature distribution shifts, and prediction confidence scores

Without this infrastructure, a model degrades undetected as market conditions evolve, client populations shift, or data pipelines introduce quality issues. By the time performance degradation is discovered through manual review, months of unreliable predictions have already been served to production users.

Security and Compliance Infrastructure

The same pipelines and models that drive predictions also handle sensitive client financial data, personally identifiable information, and proprietary trading strategies. That data exposure demands SOC 2 Type 2-compliant infrastructure across every layer. Production systems must include:

- Encryption at rest and in transit: All data storage and transmission encrypted using industry-standard protocols

- Role-based access controls: Granular permissions ensuring analysts, advisors, and compliance officers see only the data and predictions appropriate to their role

- Audit logging: Immutable records of who accessed which data, when, and what actions were taken

- Data residency compliance: Systems architected to meet jurisdictional data storage requirements

Hexaview's regulatory-aware architecture addresses these controls at the infrastructure level — embedded in the system design, not patched in after a security review surfaces gaps.

What to Look for in an AI Development Partner for Wealth Management

Domain Expertise in Capital Markets and Wealth Management Is Not Optional

A technology partner that understands the difference between time-weighted returns and money-weighted returns, how custodian data feeds are structured, and what FINRA explainability requirements mean for model design will deliver a production system that passes regulatory review and integrates with existing workflows.

Without that context, even a technically functional model fails in a regulated advisory environment — it lacks audit trails, produces unexplainable predictions, or misinterprets financial data schemas entirely.

Hexaview's WealthTech 100 recognition in 2023 by FinTech Global (which evaluates firms across a network of over 300,000 fintech professionals on industry significance, innovation, and growth) signals credibility in this space. More telling is the production record: 10+ years in capital markets and wealth management, with client relationships at firms like LPL Financial and Addepar demonstrating engagement at scale, not just in pilots.

Production Track Record, Not Just Prototypes

Ask to see a live system in operation — not a demo environment. Confirm the proposed engagement covers:

- Data pipeline construction and testing

- Model deployment on cloud infrastructure (AWS, Azure, or GCP)

- Monitoring and retraining infrastructure

- Compliance documentation and audit trail design

- Integration with existing portfolio management and CRM systems

A prototype model trained on sample data and delivered as a script is not the same as a production system handling daily custodian feeds, serving real-time predictions to hundreds of advisors, and maintaining audit logs for compliance review.

Post-Deployment Support, Model Monitoring, and Continuous Improvement

Predictive models in wealth management degrade when market regimes shift, client behavior evolves, or new data sources become available. The engagement should include:

- Defined drift monitoring thresholds: Quantitative criteria that trigger model review when input distributions or performance metrics shift

- Retraining schedules: Regular cadence for updating models with recent data and validating performance improvements

- Technical support structure: Escalation paths, response time commitments, and access to the engineering team that built the system

A one-time deployment without ongoing monitoring and retraining leaves firms running predictions on a model that is degrading against current market conditions — with no visibility into when or how badly it has drifted.

Frequently Asked Questions

What are predictive analytics in AI?

Predictive analytics in AI uses machine learning models and statistical methods to analyze historical data and forecast future outcomes: client behavior, portfolio risk, or market movements. This enables firms to act before events occur rather than reacting after the fact.

Which AI tool is widely used for predictive analytics?

Python-based ML libraries (scikit-learn, XGBoost, TensorFlow) and cloud platforms (AWS SageMaker, Azure ML) are the most common. In wealth management, XGBoost tends to dominate tabular financial data tasks because it balances interpretability with strong performance — both critical under regulatory scrutiny.

Is ChatGPT generative or predictive AI?

ChatGPT is generative AI, designed to produce new content from learned patterns, not to forecast specific outcomes from historical data. The two are complementary: predictive AI surfaces the signal, and generative AI helps communicate it.

How is predictive analytics used in portfolio management?

Predictive analytics in portfolio management forecasts portfolio drift and rebalancing needs, predicts risk factor exposures, identifies underperforming positions ahead of drawdown events, and generates forward-looking scenario analyses based on macroeconomic signals. This enables proactive rebalancing and risk management rather than reactive adjustments after thresholds are breached.

What are the main challenges of implementing predictive analytics in wealth management?

The three core challenges are: data quality across fragmented custodian and CRM systems, regulatory requirements for model explainability, and ongoing model monitoring as market conditions shift. Generic ML platforms don't address financial data schemas or compliance standards — domain-specific engineering expertise is required.