Introduction

Markets move in milliseconds. Regulatory scrutiny intensifies daily. Customer expectations have shifted from reactive service to proactive intelligence. FinTech and asset management leaders face mounting pressure to stay ahead, yet most firms remain a step behind—reacting to events rather than predicting them.

The firms winning in this environment share one common advantage: they predict what happens next. In practice, that looks like:

- Spotting credit defaults before they materialize

- Catching fraud in real time rather than after the damage is done

- Adjusting portfolios before market shifts hit

- Intervening on at-risk customers before churn becomes a fact

- Flagging regulatory exposure before auditors arrive

That gap between reacting and predicting is where this article focuses. It breaks down what predictive analytics actually means in a finance context, where it delivers the most measurable value, the pitfalls that derail implementation, and what to look for in an AI consulting partner who understands regulated financial environments.

Key Takeaways

- Predictive analytics uses historical and real-time data to forecast credit defaults, fraud, churn, and market movements—shifting financial decisions from reactive to proactive

- Key use cases span credit risk scoring, fraud detection, portfolio optimization, churn prevention, and AML compliance

- Success requires navigating data quality issues, model explainability mandates, and strict regulatory constraints unique to financial services

- Generic AI implementations frequently fail in finance—domain expertise is what bridges pilot to production

- Pairing AI depth with financial services domain expertise delivers faster time-to-value and models regulators can defend

What Is Predictive Analytics in Finance?

Predictive analytics is the use of statistical algorithms and machine learning to analyze historical and real-time data to forecast future outcomes. It differs from descriptive analytics (what happened) and diagnostic analytics (why it happened). Prescriptive analytics extends this further by recommending what to do next.

Finance is a natural fit for predictive analytics. The industry generates enormous volumes of structured transactional data, operates on probabilistic decision-making (lending, underwriting, investing), and has long relied on quantitative models. AI extends those models — making them faster, more accurate, and capable of incorporating unstructured data like news sentiment or behavioral signals.

Market context: The AI in FinTech market reached USD $36.61 billion in 2026 and is projected to grow at a 22.04% CAGR to USD $99.09 billion by 2031. This expansion is driven by demand for real-time decisioning and personalized financial services at scale. Within this market, fraud and risk management accounts for 30.55% of market share, with cloud deployment comprising 81.35% of implementations.

Consumer expectations are accelerating the shift. According to Accenture's 2025 Global Banking Consumer Study, 73% of banking customers engage with multiple banks beyond their primary institution, and 58% purchased a financial product from a new provider in the last 12 months.

Banks with the highest customer advocacy grow revenue 1.7x faster than peers. That gap is increasingly driven by real-time personalization — the kind that only predictive intelligence can deliver at scale.

High-Value Use Cases in FinTech and Asset Management

Predictive analytics applies across five high-stakes functions in FinTech and asset management — each with measurable, documented impact on revenue, risk, and operations.

Credit Risk Scoring and Loan Underwriting

Traditional credit models rely on static FICO scores and historical credit data — missing a large portion of creditworthy individuals and businesses. The CFPB's 2025 technical correction documented the scale of that gap:

- 5.8% of U.S. adults were truly credit invisible in 2010 (down from an originally reported 11%)

- 12.7% (29.7 million adults) remained unscored due to thin or stale credit files

- 9.8% (25.3 million) still lacked scoreable credit histories by 2020

AI-driven models incorporate alternative data—transaction behavior, cash flow patterns, utility payments, mobile usage—to produce more accurate and inclusive credit assessments. These models continuously retrain as new repayment data arrives, adapting to changing risk profiles in real time.

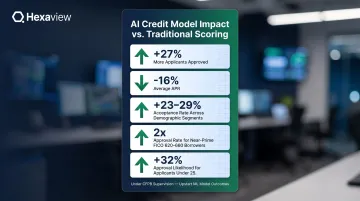

Measurable impact: Under the CFPB's first No-Action Letter, Upstart's ML/alternative data model demonstrated 27% more applicants approved, 16% lower average APRs for approved loans, and acceptance rates increased 23-29% across all tested race, ethnicity, and sex segments. Near-prime consumers (FICO 620-660) were approved approximately 2x as frequently, and applicants under 25 were 32% more likely to be approved.

Fraud Detection and Financial Crime Prevention

Rule-based fraud detection systems rely on static thresholds—flagging transactions over a certain amount or frequency. Real-time ML models learn individual behavioral baselines and flag anomalies as they occur, detecting synthetic identity fraud, account takeover, and advanced fraud schemes that rule-based systems miss.

Recent loss figures show why static systems can't keep pace:

- U.S. consumers lost $12.5 billion to fraud in 2024 — a 25% year-over-year increase

- Synthetic identity fraud crossed $35 billion in 2023, with generative AI accelerating the threat (Federal Reserve Bank of Boston)

- Account takeover fraud hit $15.6 billion in U.S. losses in 2024, up from $12.7 billion in 2023

Financial institutions deploying ML models achieve a 30-40% reduction in false positive alerts versus rule-based systems, according to Deloitte. This reduces investigator burden while improving detection precision — with 24/7 monitoring that adapts faster than human analysts can.

Portfolio Optimization and Investment Intelligence for Asset Managers

Asset managers and wealth management firms use predictive models—time series forecasting, neural networks—to anticipate market movements, optimize portfolio allocations, and manage drawdown risk. Robo-advisory platforms automate rebalancing based on predicted market conditions and investor risk profiles.

This is particularly relevant for family offices and fund services looking to scale personalized investment strategies. Predictive models enable asynchronous rebalancing across thousands of accounts, executing trades based on forecasted market conditions rather than reactive triggers. Portfolios adjust proactively rather than responding after a market move has already occurred.

That operational model is exactly what Hexaview built for a U.S. financial services client — a distributed trade and order management platform with asynchronous rebalancing architecture, modernizing legacy systems and enabling real-time, data-driven investment decisions at scale.

Customer Churn Prediction and Lifetime Value Modeling

FinTech platforms use behavioral signals—declining app activity, repeated failed transactions, reduced engagement—to identify customers at risk of churning before they leave. This enables proactive outreach or personalized retention offers.

The economics are compelling. Harvard Business Review research shows acquiring a new customer is 5 to 25 times more expensive than retaining an existing one. Increasing customer retention rates by 5% increases profits by 25% to 95%. Given that 73% of customers engage with multiple banks and 58% purchased a financial product from a new provider in the last year, churn risk is structural in modern banking.

Identifying at-risk accounts before switching occurs directly extends lifetime value — targeted retention interventions typically cost far less than acquiring replacement customers.

Regulatory Compliance and AML Monitoring

Predictive models flag suspicious transaction patterns for anti-money laundering (AML) compliance and anticipate regulatory risk exposure. Automating compliance monitoring reduces both operational cost and the risk of regulatory penalties.

The cost of financial crime compliance in the U.S. and Canada reached $61 billion annually, with 99% of financial institutions reporting compliance cost increases. AI-powered AML monitoring can increase detection rates by 50% and cut false positives by 70%, according to EY.

Model auditability is critical here. Regulators expect firms to explain why a transaction was flagged or why a decision was made—making explainability a compliance requirement, not just a technical preference.

The AI and ML Models Powering Predictive Finance

Understanding what's under the hood helps decision-makers select the right approach. These model families are often combined in production systems rather than used in isolation.

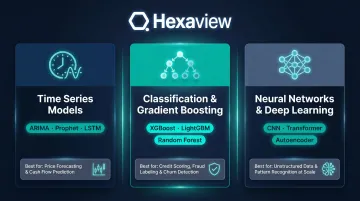

Three primary model families dominate financial predictive analytics:

Time series models (ARIMA, Prophet, LSTM networks): Best for sequential financial data like price forecasting, default prediction over time, and cash flow modeling. LSTM (Long Short-Term Memory) networks excel at capturing long-term dependencies in financial time series—essential for modeling market trends that unfold over weeks or months.

Classification models and gradient boosting methods (e.g., XGBoost): Widely used for credit scoring, fraud labeling, and churn classification because of their accuracy and interpretability. XGBoost handles large datasets efficiently and produces feature importance scores that help explain model decisions—critical in regulated environments.

Neural networks and deep learning: Handle large, complex, unstructured datasets like transaction logs combined with behavioral signals. Used in market prediction and pattern recognition at scale. VisaNet plus AI prediction accuracy reaches 98% in fraud detection, showing what deep learning can achieve at production scale.

In regulated financial environments, explainability isn't optional. "Black box" models create real compliance exposure: lenders and investment advisors must justify model decisions to regulators and customers. Under ECOA, creditors cannot deny credit applications without providing specific, articulable reasons—reasons a model must be able to produce.

Regulators have formalized these expectations. The Federal Reserve, FDIC, and OCC rescinded SR 11-7 in April 2026, replacing it with a principles-driven model risk management framework that explicitly addresses AI/ML. Compliance-by-design—building audit trails, explainability, and bias testing into the model pipeline from day one—is now a baseline regulatory requirement.

Implementation Challenges in Regulated Financial Environments

The gap between a predictive analytics proof-of-concept and a production-grade system trusted by compliance teams, risk officers, and customers is wider in FinTech and asset management than in most other industries. Here are the four most common failure points.

Data Quality and Integration Complexity

Financial data typically lives across siloed systems—core banking platforms, CRMs, market data feeds, legacy infrastructure. Data is often inconsistent, incomplete, or formatted differently across sources. Poor data quality directly degrades model accuracy.

Data governance practices required before modeling can begin:

- Validation pipelines that verify data completeness and accuracy

- Standardization across disparate sources (account numbers, transaction codes, customer identifiers)

- Enrichment with alternative data sources where internal data is insufficient

- Automated daily data loads and backups to ensure consistency

Hexaview's work with a leading wealth tech firm illustrates this challenge. The client faced fragmented data across multiple custodians (LPL, Fidelity, ORION). After implementing a unified data lake with streamlined data-load processes, the firm achieved +60% data accessibility, +75% analytical accuracy, and -50% reduction in manual effort.

Regulatory Compliance and Model Governance

Financial AI models face regulatory scrutiny that most other industries do not. Credit models must comply with fair lending laws (e.g., ECOA in the US), fraud systems must meet AML/KYC requirements, and investment tools face fiduciary standards.

The U.S. Treasury's December 2024 report on AI in financial services identified three compounding pressures: a supervision gap between banks and fintechs, fragmented state-level AI and privacy laws (CA, CO, NY), and concentration risk from a small number of foundation model providers. Keeping models compliant as that regulatory landscape shifts is the central challenge.

Compliance-by-design is more effective than retrofitting compliance after deployment:

- Build audit trails into model pipelines from the start

- Implement explainability tools that show which features drive model outputs

- Conduct bias testing as part of model validation, not as an afterthought

- Establish model tiering and proportional governance based on risk

Firms that work with SOC 2 Type 2-certified partners who already have financial services compliance frameworks in place reduce both implementation time and audit exposure. Hexaview's decade-plus experience across capital markets and wealth management means compliance architecture is built into the engagement from day one—not bolted on after a regulator asks questions.

Bias Detection and Fairness

Models trained on historical financial data can perpetuate existing lending or investment biases. Bias in credit scoring models can trigger CFPB enforcement actions and class-action exposure.

Practices needed to detect and mitigate bias:

- Use diverse training datasets that reflect the full customer population

- Conduct regular fairness audits across protected classes (race, gender, age)

- Track disparate impact metrics continuously, not just at model launch

- Monitor performance across demographic segments post-deployment and retrain when drift appears

Upstart's model, tested under CFPB supervision, demonstrated that alternative data models can increase fairness when properly designed—achieving acceptance rate increases and APR reductions across all tested demographic segments without creating actionable fair lending disparities.

Legacy System Integration and Change Management

Legacy core banking and portfolio management systems were never designed for real-time, API-driven data exchange. Deploying modern AI infrastructure alongside them is a practical challenge most firms underestimate going in.

Approaches that work:

- API gateway layers that expose legacy system data without requiring core system rewrites

- Microservices architecture that decouples AI/ML components from monolithic legacy platforms

- Phased modernization that allows institutions to extract AI value without a full platform overhaul

User adoption is just as likely to kill a deployment as a technical failure. Risk officers who don't understand a model's logic will route around it; loan officers under pressure will default to gut instinct. Implementations that stick include stakeholder engagement from day one, transparent model documentation, and structured training that gives decision-makers enough context to trust the output.

Why Domain-Specific AI Consulting Drives Better Outcomes

Implementing predictive analytics in FinTech and asset management is not a pure technology problem. It requires deep familiarity with financial data structures, regulatory environments, risk frameworks, and the specific business logic of credit, investment, and compliance workflows.

A generalist AI firm building its first financial model is unlikely to anticipate the compliance requirements, data nuances, or stakeholder concerns that derail projects. The numbers bear this out: McKinsey found that 80% of companies use latest-generation AI, yet 80% report no significant financial gains. MIT research found 95% of GenAI pilots fail to accelerate revenue.

What to look for in an AI consulting partner for financial services:

- Demonstrated experience with capital markets or wealth management workflows—not just generic ML delivery

- Security posture that matches financial services requirements (SOC 2, data governance frameworks)

- Ability to deliver systems that work in live environments, not just prototypes

- Track record with comparable clients in regulated environments

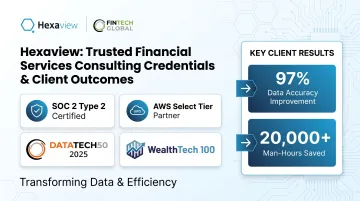

Hexaview Technologies checks each of these boxes. With over 10 years of experience in capital markets and wealth management, the firm holds SOC 2 Type 2 certification and AWS Select Tier Partner status, and is recognized on the WealthTech 100 and DATATECH50 lists.

For clients like LPL Financial and Addepar, Hexaview has delivered measurable results: a 97% improvement in data accuracy and over 20,000 man-hours saved in analysis.

The practical impact of having a consulting partner with financial domain depth:

- Faster time-to-value because the team understands the data and regulatory context from day one

- Fewer costly rework cycles because compliance and explainability requirements are built in

- More defensible models because they reflect actual financial risk logic—not generic ML pattern-matching applied to financial data

Hexaview's hybrid onsite-offshore model supports cost-effective scaling without sacrificing compliance. U.S.-based client engagement pairs with offshore development centers that accelerate delivery while meeting the security standards regulated financial environments require.

What's Next: From Predictive to Prescriptive Analytics in Finance

Predictive analytics answers "what will happen." Prescriptive analytics answers "what should we do about it."

Prescriptive systems don't just forecast churn or credit default—they recommend and, increasingly, execute specific actions autonomously through agentic AI workflows:

- Offering optimal loan terms to at-risk borrowers before they churn

- Triggering portfolio rebalancing moves within predefined risk limits

- Routing customer retention interventions to the right team at the right time

Agentic AI takes this further. AI systems can now monitor portfolios, flag risks, initiate compliance alerts, and adjust positions within predefined guardrails—without requiring human sign-off at every step. This shift from reporting to autonomous action is already underway in treasury management, algorithmic trading, and compliance monitoring.

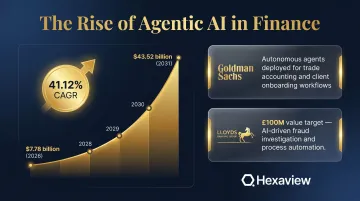

The agentic AI in financial services market is valued at $7.78 billion in 2026, growing at a 41.12% CAGR to reach $43.52 billion by 2031—a growth rate nearly double the broader AI in FinTech market.

Two early deployments illustrate the pace:

- Goldman Sachs partnered with Anthropic to build autonomous agents for trade accounting, client due diligence, and onboarding—aiming to cut time-to-completion for core operations

- Lloyds Banking Group expects £100 million in value from agentic AI in 2026, deploying systems for fraud investigations and complex complaints

Firms building their predictive analytics foundations now will be positioned to adopt agentic capabilities as they mature. Data quality, model governance, and clean integration layers aren't just prerequisites for prediction—they're the scaffolding that makes autonomous action safe enough to deploy at scale.

Frequently Asked Questions

What is predictive analytics in finance?

Predictive analytics applies machine learning and statistical models to historical and real-time financial data to forecast outcomes such as credit defaults, fraud events, market movements, or customer churn. This enables more proactive, data-driven decision-making across lending, investment, compliance, and customer engagement.

How is predictive analytics used in finance?

Primary applications include credit risk scoring and loan underwriting, real-time fraud detection, portfolio optimization for asset managers, customer churn prediction, and regulatory compliance monitoring. Each application relies on models trained on historical financial data and continuously updated with new inputs to maintain accuracy.

What are the three different types of predictive analytics?

The three types are:

- Predictive modeling — forecasting future outcomes from historical patterns

- Machine learning classification — categorizing outcomes such as fraud vs. non-fraud

- Time series forecasting — predicting values like stock prices or loan defaults over time

Financial applications routinely combine all three to apply multiple analytical methods at once.

What are the 4 types of business analytics?

The four types are descriptive (what happened), diagnostic (why it happened), predictive (what will happen), and prescriptive (what should be done). FinTech and asset management firms are increasingly moving from descriptive toward predictive and prescriptive capabilities to drive proactive decisions rather than reactive responses.

What are the four types of FinTech?

The four main FinTech segments are digital payments and banking, lending and credit technology, investment and wealth management technology (WealthTech), and insurance technology (InsurTech). Predictive analytics plays a critical role across all four, with particularly deep applications in lending, WealthTech, and payments fraud prevention.

How do FinTech and asset management firms successfully implement predictive analytics?

Successful implementation depends on four foundations:

- Governed data — high-quality, well-structured data as the starting point

- Explainable models — balancing accuracy with regulatory transparency requirements

- API integration — connecting models to existing infrastructure without full rearchitecting

- Domain-expert partners — consultants with both AI engineering depth and financial services experience

Building compliance into the model pipeline from day one prevents costly retrofitting later.