Introduction

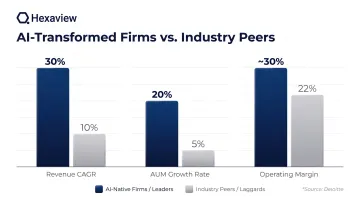

Wealth management firms that have merely "digitized" by bolting AI tools onto legacy systems are losing clients and advisors to AI-native challengers who embedded intelligence into core workflows from the start. The gap goes far deeper than technology choices. AI-native competitors don't automate around existing processes—they redesign entire workflows around machine learning, autonomous decision-making, and continuous data optimization. According to Deloitte's enterprise transformation study, top-performing digitally transformed wealth firms triple their peers' revenue CAGR, grow AUM at 4x the rate, and achieve operating margins near 30% compared to peers' 22%.

The market opportunity is substantial. PwC projects global AUM will climb from $139 trillion in 2024 to $200 trillion by 2030 at a 6.2% CAGR, while the wealth management software market is expanding from $6.28 billion in 2025 to $18.77 billion by 2033 at 14.7% annually.

Most firms are squandering it. McKinsey finds relationship managers spend 60-70% of their time on non-revenue activities, fragmented data silos block personalization, and compliance costs consume an average of 19% of revenues.

The client base is shifting, too. Younger HNWI clients inheriting $83.5 trillion through 2048 expect personalized, digital-first experiences — and over 70% of heirs fire their inherited advisor when those expectations aren't met.

Robo-advisors have already crossed $1 trillion in AUM and keep gaining share at rates traditional advisory models can't match. The competitive pressure is coming from multiple directions simultaneously.

This article explains what AI-native transformation means in practice, which use cases deliver measurable ROI, and a practical 4-stage roadmap for implementation — so firms can move from managing legacy friction to building durable competitive advantage.

Key Takeaways

- AI-native transformation rebuilds workflows with AI at the foundation, not layered onto legacy systems

- Hyper-personalized journeys, AI workspaces, automated compliance, and intelligent analytics are delivering documented ROI

- The 4-stage journey: Data Foundation, Use Case Prioritization, Platform Integration, Continuous Intelligence

- Transformed firms report 3x revenue CAGR, 4x AUM growth, and ~30% operating margins vs. 22% for peers

- Data quality gaps, compliance risks, and cultural resistance are all manageable with a phased, governed rollout

Why Legacy Approaches Are Failing Wealth Managers Right Now

The "administrative tax" is draining advisor productivity at the source. Relationship managers burn 60-70% of their time on non-revenue-generating activities—onboarding paperwork, compliance documentation, manual data assembly across siloed systems. Every hour spent reconciling custodian feeds is an hour not spent deepening client relationships or sourcing new business.

Legacy platforms designed in the pre-cloud era make this worse. The integration problem is well-documented:

- 94% of firms report limited technology integration creates productivity challenges

- 57% cite lack of integration between core apps as their top technology pain point

- Advisors drowning in admin deliver generic service — and margins erode accordingly

A client expectation gap is widening the generational fault line. Younger HNWIs and the mass affluent—who will inherit $124 trillion through 2048—grew up on Amazon, Spotify, and real-time mobile banking. They expect instant portfolio visibility, ESG-aligned options surfaced proactively, and onboarding measured in minutes.

The data on what's at stake is stark:

- Over 70% of heirs fire their parents' advisor after inheritance, often because the digital experience feels decades behind consumer apps

- CFA Institute research shows 90%+ of Gen Z and millennial wealthy investors use paid financial advice

- Yet 43% of Gen Z access robo-advice only — they want human guidance, delivered digitally

Firms that can't provide both lose the next generation before the wealth even transfers.

Competitive pressure from FinTechs and robo-advisors has moved from theoretical to existential. The robo-advice industry surpassed $1 trillion in AUM in 2023, with Vanguard's Personal Advisor platform holding $206.6 billion and Schwab Intelligent Portfolios managing $80.9 billion. These platforms didn't retrofit AI—they architected around it, achieving client acquisition costs and operational efficiency traditional firms can't match with advisor-led models alone.

Talent retention is under the same pressure. 51% of advisors say lack of better tech would cause them to leave their firm. AI-native competitors are positioned to capture both clients and advisors faster than legacy firms can modernize.

What AI-Native Digital Transformation Really Means (And Why It's Different)

"Digitizing" a process means making it electronic. "AI-native transformation" means redesigning the process around AI decision-making, automation, and continuous learning from the ground up. The distinction is architectural, not incremental.

Consider onboarding: digitizing means moving PDF forms online. AI-native onboarding uses intelligent data capture that pre-fills fields from document scans, real-time identity verification APIs, and a risk-profiling engine that auto-generates investment recommendations before the advisor's first call. The client experiences speed and personalization; the advisor enters the relationship armed with insights, not blank forms.

An AI-native platform in wealth management requires three foundational elements:

- Unified data architecture — no siloed CRMs, portfolio systems, and custodian feeds operating independently

- Machine learning models embedded in core workflows, not in dashboards you check occasionally

- AI agents that execute tasks autonomously within compliance guardrails, not chatbots that answer FAQs

If your "AI strategy" is a business intelligence tool bolted onto existing systems, you're digitizing, not transforming. AI-native means the system learns from every client interaction, refines recommendations continuously, and automates decision logic that previously required human intervention.

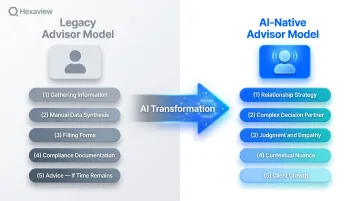

The advisor role fundamentally shifts. In legacy models, advisors gather information, synthesize data manually, fill forms, and then—if time remains—provide advice. In AI-native models, the advisor transitions from information gatherer to relationship strategist and trusted decision partner. AI handles data synthesis, portfolio drift monitoring, compliance documentation, and next-best-action recommendations. The human provides judgment, empathy, and contextual nuance machines can't replicate. 96% of advisors believe generative AI can revolutionize wealth management, and 51% are already using it—yet most firms haven't redesigned workflows to capitalize on this shift.

For FinTech companies, AI-native transformation means building products where AI powers core differentiation, not decorative features. Algorithmic underwriting that approves loans in seconds, dynamic risk scoring that updates in real time based on behavioral signals, personalized product recommendations triggered by life events—these capabilities define the product, not supplement it. If your AI can be removed without breaking the product, it's not AI-native.

That capability depth comes with a governance requirement. In financial services, every AI model must be explainable, auditable, and compliant with evolving regulations: the EU AI Act classifies credit scoring AI as high-risk, and FINRA issued GenAI guidance requiring firms to maintain oversight over AI-driven processes. Explainability and human-in-the-loop oversight are design requirements from day one, not afterthoughts. Firms that architect compliance into AI from the start scale faster than those that retrofit governance later.

Key AI Use Cases Reshaping Wealth Management and FinTech

Hyper-Personalized Client Journeys

AI-powered customer data platforms merge transaction history, behavioral signals, life event triggers, and risk profiles to generate proactive, contextually relevant recommendations rather than generic product pushes timed to quarterly reviews. A client nearing retirement automatically receives a rebalancing recommendation before their advisor calls, not after.

The system detects the trigger (age, portfolio composition, spending patterns), models the optimal adjustment, and surfaces it to the advisor with supporting rationale. The client experiences foresight; the advisor delivers value without manual monitoring.

AI compresses onboarding from a multi-week paperwork ordeal into a focused digital experience. Intelligent forms adapt based on responses: if a client indicates they're a business owner, the system surfaces questions about entity structure and succession planning. Key automation capabilities include:

- Real-time KYC/AML verification that checks identity, sanctions lists, and PEP status instantly

- Automatic risk profile generation that recommends portfolio allocations before the first advisor meeting

- Compliance documentation that updates in parallel, reducing back-and-forth

Onboarding compresses from weeks to days while improving both compliance accuracy and client satisfaction.

AI-Augmented Advisor Workspaces

The unified advisor workspace aggregates client portfolio data, CRM history, market signals, and next-best-action recommendations into a single interface. Advisors enter client meetings fully briefed by AI, not scrambling to assemble information from five systems.

The workspace displays portfolio drift alerts, upcoming tax events, recent transactions, and suggested talking points, all contextualized for that specific client. Preparation time drops from an hour to minutes, and meeting quality improves because advisors focus on strategy, not data retrieval.

Agentic AI capabilities take this further. AI agents autonomously prepare meeting briefs, flag portfolio drift, draft client communications, and initiate compliance documentation—freeing advisors to focus on the 20-30% of high-value activities that drive retention and AUM growth. The agent doesn't wait for prompts. It monitors continuously and surfaces insights when they matter. An advisor managing 100 clients can deliver personalized service at scale without adding headcount.

Automated Compliance and Risk Monitoring

AI-native compliance tools perform continuous real-time monitoring of portfolio positions, client communications, and transaction patterns against regulatory rules—replacing periodic manual reviews with always-on surveillance. The system flags potential violations before they occur, not months later during an audit. Compliance costs average 19% of annual revenues, and regulatory activity hours have risen 61% since 2016. McKinsey reports AI delivers 20-30% reductions in quality assurance costs by automating transcript monitoring and flagging violations in real time. Compliance shifts from reactive overhead to predictive risk management.

Intelligent Portfolio Analytics

AI-driven analytics enable advisors to manage complex, holistic portfolios at scale without expanding their teams proportionally. Capabilities include:

- Multi-asset performance attribution across public equities, fixed income, alternatives, and illiquid holdings

- Scenario modeling that stress-tests portfolios against market shocks, interest rate changes, or geopolitical events

- ESG data integration that surfaces alignment gaps and suggests rebalancing to meet client values

- Exposure analysis across asset classes, geographies, and risk factors—including illiquid and alternative investments

With these tools, advisors shift from explaining last quarter's performance to modeling the scenarios that will shape the next one.

The 4-Stage Roadmap to AI-Native Transformation

Stage 1 — Assess and Build the Data Foundation

Most transformation failures trace back to data. Siloed, incomplete, or low-quality data makes every downstream AI model unreliable. If client data lives in separate CRM, portfolio management, and custodian systems with no unified identity layer, AI can't deliver personalized insights: it's working from fragments, not a full picture. Stage 1 involves:

- Auditing existing data assets: catalog every system, data source, and integration point

- Establishing unified data governance: define data ownership, quality standards, and access policies

- Investing in integration infrastructure: build data pipelines, APIs, and identity resolution before selecting AI tools

This stage feels unglamorous but is non-negotiable. Firms that rush to AI pilots without fixing data foundations waste money on models that can't scale.

Stage 2 — Prioritize High-Value AI Use Cases

Start narrow. Identify 2-3 use cases with the highest pain points and clearest ROI—typically client onboarding acceleration, advisor productivity enhancement, or compliance automation. Run time-bound pilots (90-120 days) with defined success metrics:

- Onboarding: reduce time-to-first-trade from 14 days to 3 days

- Advisor productivity: cut meeting prep time from 60 minutes to 15 minutes

- Compliance: reduce exception rates from 5% to 1%

Define these metrics before launch, not after. Pilots without clear KPIs become perpetual experiments. Prioritize use cases where manual processes are both high-cost and high-frequency—those deliver fastest ROI and build organizational confidence.

Stage 3 — Integrate AI Into the Core Platform

Transitioning from pilot to production requires selecting AI-compatible platforms: cloud-native, API-first architecture that integrates with CRM systems and data aggregation layers. Deploy models that operate within explainable, auditable guardrails, where every recommendation traces back to source data and decision logic for regulatory review.

Hexaview's AI Engineering and Salesforce/Agentforce expertise supports firms at this stage. The approach covers:

- Agentforce-powered automation with built-in compliance guardrails for wealth management workflows

- Unified data architecture that eliminates siloed systems

- Embedded machine learning models in core workflows (not just analytics dashboards)

- AI agents that execute tasks autonomously within regulatory boundaries

With SOC 2 Type 2 certification and over 10 years of capital markets expertise, Hexaview delivers transformation that is both high-performance and audit-ready.

Stage 4 — Scale, Measure, and Continuously Improve

AI-native transformation isn't a project with an end date: it's an operating model. Stage 4 involves:

- Retrain models quarterly (or as performance drifts) to account for shifting markets and client behaviors

- Track KPIs that evolve with the business: adoption rates and time savings early on, AUM growth and revenue per advisor as the program matures

- Apply proven models to new client segments, products, and workflows once initial use cases are validated

The human element ultimately determines success. Technology without culture change delivers a fraction of its potential. Transformation requires executive sponsorship, cross-functional collaboration between business and technology teams, and clear communication to advisors that AI augments their value, not replaces it.

Firms that celebrate early wins, invest in reskilling, and tie incentives to adoption succeed. Those that mandate tools without explaining the "why" face sustained resistance.

Top Challenges in AI-Native Transformation and How to Address Them

Legacy Integration Complexity

Legacy integration complexity is the most common blocker. Most wealth management firms operate on monolithic core systems built decades ago, with proprietary data formats and minimal API connectivity. Attempting a "big bang" migration creates unacceptable business risk.

The solution is a modular, composable architecture strategy — replacing or wrapping legacy components incrementally. Prioritize integration sequencing by business value:

- Client-facing systems first (onboarding, portals) to deliver immediate client experience improvements

- Advisor tools second (workspaces, analytics) to drive productivity gains

- Back-office systems last (accounting, custodian reconciliation) once front-office ROI is proven

This approach reduces risk, demonstrates value early, and funds later stages with savings from earlier wins.

Regulatory and Compliance Risk

Regulatory risk intensifies when AI touches financial advice. The EU AI Act classifies credit scoring and financial AI as high-risk, requiring explainability and human oversight. FINRA's Regulatory Notice 24-09 confirms that all existing rules apply to AI just as to any other technology.

Firms must involve legal, compliance, and risk teams from the earliest design stages — not brought in at the end to review finished systems, but embedded as co-architects building compliance in from the start. Zero-trust data security, model explainability, and audit trails are regulatory requirements, not optional features.

Talent and Cultural Resistance

Even when the technology works, talent and cultural resistance can derail transformation entirely. Wealth management professionals who built careers on relationship management and manual expertise often perceive AI as an existential threat. Firms must address this directly:

- Invest in reskilling programs that teach advisors to use AI tools effectively

- Demonstrate early wins that free advisors from administrative drudgery, giving them more client face time

- Tie performance incentives to adoption of new workflows, not just AUM or revenue targets

- Communicate consistently that AI makes advisors more valuable, not obsolete

Resistance fades when advisors see peers closing more business, spending less time on paperwork, and delivering better client outcomes using AI tools.

Measuring Success: KPIs and Business Outcomes of AI-Native Transformation

Operational KPIs track how well transformation improves day-to-day execution:

- Advisor time on high-value activities (client meetings, strategic planning) vs. admin work—target 70%+ on high-value, down from typical 30-40%

- Client onboarding time reduction—from weeks to days; 22% of advisors rank onboarding as #1 tech investment priority

- Compliance exception rate—reduce manual errors and regulatory flags by 50%+

- Portfolio analytics coverage—percentage of AUM with real-time exposure analysis, including illiquid assets

- Data accuracy improvement—unified data platforms eliminate reconciliation errors

These operational gains translate directly into financial performance. McKinsey reports AI delivers 30-45% cost reductions in customer operations through automation, including 10-15% workforce optimization and 25-40% call reduction through root-cause analysis.

Business-outcome KPIs connect transformation to financial performance:

- Revenue per advisor—AI-augmented advisors manage more clients at higher service levels

- AUM growth rate—better client experiences and proactive recommendations drive retention and referrals

- Client retention rate—personalized journeys reduce attrition, especially among younger clients

- Net new client acquisition cost—digital onboarding and automated marketing lower CAC

- Revenue CAGR vs. peers—the ultimate competitive benchmark

Deloitte's research on digitally transformed wealth firms quantifies the gap: top performers triple their peers' revenue CAGR, grow AUM at 4x the rate, and achieve operating margins near 30% compared to 22% for laggards. At that scale, the gap between leaders and laggards becomes self-reinforcing: better margins fund further investment, while slower firms fall further behind.

Hexaview's AI Engineering and Data Science practice has delivered documented outcomes for wealth management clients, including a 97% rise in data accuracy and 20,000+ man hours saved in analysis. With SOC 2 Type 2 certification and over 10 years of capital markets expertise, Hexaview ensures transformation delivers both performance and audit-ready governance. Explore Hexaview's FinTech and wealth management solutions.

Frequently Asked Questions

What is a digital wealth manager?

A digital wealth manager uses technology—AI, automated analytics, digital portals—to deliver investment advice and portfolio management at scale. This includes both digital self-service capabilities (robo-advisors) and AI-augmented human advisor interactions that blend automation with personal guidance.

What are the 4 stages of digital transformation?

The four stages of digital transformation in wealth management are:

- Assess and Build the Data Foundation — establish unified, high-quality data infrastructure

- Prioritize High-Value AI Use Cases — pilot 2-3 use cases with clear ROI

- Integrate AI Into Core Platforms — deploy models with compliance guardrails into production

- Scale and Continuously Improve — expand AI capabilities across segments and continuously retrain models

The four stages of digital transformation in wealth management are:

- Assess and Build the Data Foundation — unify data infrastructure and establish quality standards

- Prioritize High-Value AI Use Cases — pilot 2-3 use cases with measurable ROI

- Integrate AI Into Core Platforms — deploy models with compliance guardrails into production

- Scale and Continuously Improve — expand AI capabilities across client segments and retrain models over time

Is AI going to take over wealth management?

No. AI augments advisors rather than replacing them, handling data synthesis, compliance monitoring, and routine tasks so advisors can focus on judgment, empathy, and complex planning. These human capabilities remain irreplaceable. The real threat is AI-native firms capturing clients faster than legacy firms can adapt.

How to evaluate digital transformation?

Evaluate against both operational KPIs (advisor productivity, onboarding time, compliance error rates) and business outcomes (AUM growth, revenue per advisor, client retention). KPIs should evolve dynamically as transformation matures—early-stage metrics track adoption and efficiency; later-stage metrics track competitive performance and financial results.

What are the 4 stages of wealth management?

The traditional four stages are wealth accumulation (earning and saving), wealth preservation (protecting assets), wealth distribution (retirement income), and estate transfer (legacy planning). AI-native platforms let advisors manage clients across all four stages simultaneously, rather than in siloed conversations triggered by age or life events.