The stakes are measurable. The global AI in fintech market reached $27 billion in 2024 and is projected to hit $79.4 billion by 2030, growing at a 19.7% CAGR. Companies that delay adoption risk losing ground to AI-native competitors who are already automating underwriting, fraud detection, and customer service at scale. This article covers the most impactful AI use cases for fintech startups and neo banks, key automation solutions, real implementation challenges, and how to select the right AI consulting partner.

TLDR:

- 78% of financial firms are implementing GenAI, with fintech startups reporting 86% success rates versus 68% for incumbents

- AI credit scoring approves 44% more borrowers at 36% lower APRs versus traditional models

- Automated KYC onboarding can reduce processing time by 90%, cutting customer acquisition costs significantly

- Build-in-house requires scarce ML talent; partnering with certified AI consultants delivers faster ROI with lower overhead

- 70% of financial services firms report AI talent gaps, making specialized consulting partnerships critical

Why FinTech Startups & Neo Banks Can't Afford to Delay AI Adoption

Fintech startups and neo banks face unique pressures that make AI adoption urgent rather than optional. Unlike legacy banks with physical branches to fall back on, digital-first financial services companies operate entirely through mobile apps and web platforms. The operating constraints are unforgiving:

- Managing compliance-heavy operations with lean teams

- Meeting mobile-first user expectations for instant, frictionless service

- Sustaining pressure to reduce customer acquisition cost (CAC) and churn simultaneously

78% of financial firms are currently implementing Generative AI for at least one use case, according to the U.S. Department of the Treasury. Financial services ranks among the top three industries showing the strongest AI adoption and ROI results. The gap is notable: 86% of fintech firms report measurable gains from AI, compared to just 68% of traditional incumbent firms — agile, digital-first companies consistently extract more value from AI investments than their legacy counterparts.

The cost of inaction is real. AI-native competitors are already automating credit decisions in minutes, detecting fraud in milliseconds, and delivering 24/7 personalized financial coaching without scaling headcount. For startups and neo banks, AI consulting and automation are the practical levers for competing at scale — faster onboarding, sharper risk decisions, and personalized service delivered by smaller, more efficient teams.

Top AI Use Cases for FinTech Startups & Neo Banks

Fraud Detection & Real-Time Risk Monitoring

ML-powered fraud detection goes beyond static rule-based systems by identifying anomalous transaction patterns, account behavior, and emerging threat vectors in real time. Instead of flagging transactions based on fixed thresholds, machine learning models learn normal behavior for each customer and adapt to new fraud tactics as they emerge. This reduces false positives (which frustrate legitimate customers) while catching more fraud.

For neo banks operating without physical branch oversight, real-time fraud detection is foundational. Identity fraud losses reached $27.2 billion in 2024, a 19% year-over-year increase, with account takeover fraud accounting for $16 billion of that total.

Critical fraud scenarios for neo banks include:

- Synthetic identity fraud during digital onboarding, where attackers fabricate identities using real and fake data

- Card-not-present fraud, which saw an 8% increase in 2024 affecting over 3,300 US financial institutions

- AML transaction monitoring to detect money laundering patterns across customer accounts

- Account takeover via credential stuffing and phishing attacks targeting mobile banking users

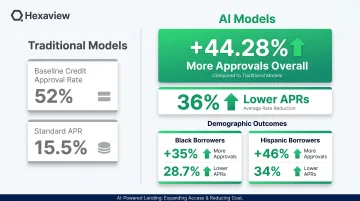

AI-Powered Credit Scoring & Underwriting

AI credit scoring models analyze hundreds of alternative data signals beyond traditional FICO scores—transaction behavior, bill payment history, device data, employment patterns, and spending habits. This enables neo banks and lending startups to approve more creditworthy customers who are underserved by legacy models.

The impact is measurable. Upstart's AI model approves 44.28% more borrowers than traditional credit-score-only models at 36% lower APRs. For Black borrowers, the model approves 35% more with 28.70% lower APRs; for Hispanic borrowers, 46% more with 34% lower APRs.

While traditional lenders may take days to review applications manually, AI-powered underwriting delivers credit decisions in minutes. That speed translates directly into higher conversion rates, better customer experience, and lower operational costs for fintech lenders.

Regulatory Compliance Automation (KYC/AML)

KYC (Know Your Customer) and AML (Anti-Money Laundering) compliance is one of the most resource-intensive operations for any fintech startup seeking a banking license or payments charter. Identity verification, document extraction, sanctions screening, and SAR (Suspicious Activity Report) filing consume disproportionate time and budget for early-stage companies—AI can automate all of it at a fraction of the manual cost.

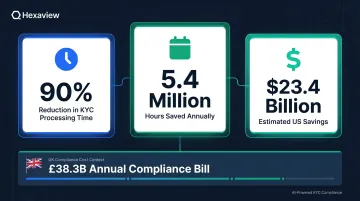

UK banks and fintechs spend approximately £21,400 per hour fighting financial crime, pushing the UK's total annual compliance bill to £38.3 billion. Potential US savings from AI-powered compliance solutions are estimated at $23.4 billion.

Beyond cost reduction, AI-powered RegTech lowers the risk of regulatory fines and makes compliance scalable as startups enter new markets. Juniper Research estimates that AI automation of KYC checks can reduce time required by 90%, generating estimated time savings of 5.4 million hours.

Personalized Customer Experience & AI Chatbots

Neo banks can deploy conversational AI (NLP-powered virtual assistants) to handle 24/7 customer support, proactive financial coaching, transaction dispute resolution, and contextual product recommendations—without scaling headcount in lockstep with users.

The cost case is clear. Chatbots deliver approximately $8 billion per year in cost savings across the financial industry, approximately $0.70 saved per customer interaction. 100% of the top 10 largest US commercial banks have deployed chatbots, and approximately 37% of the US population (over 98 million users) interacted with a bank's chatbot in 2022.

However, implementation quality matters. The same CFPB report noted that 80% of consumers who interacted with a chatbot felt more frustrated afterward, and 78% needed to connect with a human representative after chatbot failure. Getting it right means designing clear escalation paths to live agents, not just deploying a bot and walking away.

Predictive Analytics & Investment Intelligence

Fintech startups offering investment, savings, or wealth features can use ML-based predictive analytics to forecast user behavior (churn risk, product affinity), optimize portfolio suggestions, and detect early signals of financial distress to offer proactive interventions.

Predictive models enable neo banks to:

- Identify customers at risk of churning before they close accounts

- Recommend savings products based on spending patterns and financial goals

- Detect early warning signs of financial difficulty and offer budget coaching

- Optimize cross-sell and upsell timing for higher conversion rates

- Personalize investment recommendations based on risk tolerance and behavior

AI Automation Solutions That Power Neo Bank Operations

Customer Onboarding & Identity Verification Automation

End-to-end onboarding automation combines AI document processing (OCR + computer vision), biometric verification, and real-time sanctions screening to compress customer onboarding from days to minutes. For mobile-first neo banks, every extra step in the signup flow raises abandonment rates — so speed here is a direct revenue lever.

Automated onboarding delivers:

- Instant document verification using computer vision to validate IDs, passports, and proof of address

- Biometric identity checks via facial recognition and liveness detection to prevent fraud

- Real-time sanctions screening against OFAC, UN, and EU watchlists

- Automated risk scoring to flag high-risk applications for manual review

The result: shorter manual review queues, lower KYC operational costs, and a fully auditable compliance trail.

Back-Office & Accounting Workflow Automation

Lean fintech finance teams spend disproportionate time on back-office work that's both error-prone and low-value. AI-powered automation handles the heavy lifting across:

- Accounts payable and receivable processing

- Bank reconciliation and period-end close

- Automated P&L compilation

- Invoice processing and approval workflows

Hexaview's work with financial services clients demonstrates the scale of efficiency gains possible. In one engagement, automated workflow implementation saved over 250 man-hours through single-click task assignment, increased reporting accuracy, and easy monitoring capabilities. More broadly, Hexaview has documented 20,000+ man-hours saved in analysis through comprehensive back-office automation.

With routine reconciliation handled automatically, finance teams redirect their capacity toward forecasting, modeling, and growth decisions — work that actually moves the business forward.

Intelligent Financial Reporting & Reconciliation

Agentic AI and GenAI-powered reporting tools can auto-generate regulatory filings, management reports, and audit-ready documents by pulling from multiple data sources. This can cut period-end close from weeks to days, reducing the manual burden on finance and compliance teams.

Automated financial reporting enables:

- One-click regulatory reports formatted to meet specific regulatory requirements

- Real-time management dashboards instead of month-end manual compilation

- Audit trail automation with full lineage tracking for compliance

- Multi-source data consolidation from banking cores, payment processors, and CRM systems

AI-Driven Customer Support Automation

Neo banks can build tiered AI support systems to optimize cost per resolution while maintaining service quality:

- Tier 1: Handled entirely by NLP chatbots for balance inquiries, transaction history, card disputes, and password resets

- Tier 2: AI assists human agents with real-time suggestions, context from previous interactions, and recommended next actions

- Tier 3: Complex escalations handled by specialists with full AI-generated case summaries

Neo banks that deploy this tiered model typically see support volume scale 3-5x without adding equivalent headcount — keeping response times fast as the customer base grows.

What AI Consulting Delivers: Key Benefits for FinTech Companies

Financial services firms report an average 20% productivity gain across AI use cases, according to Bain & Company's 2024 survey. For startups with leaner cost structures, these gains compound: every percentage point of efficiency improvement has outsized impact on runway and profitability.

AI enables fintech startups to move from reactive to predictive decision-making. Fraud detection shifts from post-incident review to real-time pattern flagging. Credit decisions that once required manual review get scored and recommended instantly. That predictive edge translates directly into smarter capital allocation and a roadmap built on data, not gut instinct.

Those internal efficiency gains also change how fintechs compete externally. AI-powered personalization and measurable fraud reduction become capabilities that show up in product reviews, NPS data, and investor decks — not just internal dashboards.

For neo banks up against legacy institutions and well-funded competitors alike, specific outcomes matter more than general claims. Metrics like 40% faster onboarding or 25% fraud reduction strengthen fundraising conversations, sharpen market positioning, and give growth teams a concrete story to tell.

The benefits AI consulting delivers tend to cluster around three areas:

- Operational efficiency — automating credit scoring, KYC, and compliance workflows to reduce manual overhead

- Risk reduction — real-time fraud detection and model-driven underwriting that cut exposure before losses occur

- Competitive positioning — personalization at scale and faster onboarding that directly influence user acquisition and NPS

Common AI Implementation Challenges (And How to Solve Them)

Data Quality, Integration & Infrastructure Gaps

AI models are only as good as the data pipelines feeding them. Many fintech startups lack clean, consolidated data architectures, especially when customer and transaction data sits across multiple third-party APIs, payment rails, and cloud services.

Solution: Establish an ETL pipeline and unified data lake early. Use cloud-native integration services (AWS Glue, Azure Data Factory, or Google Cloud Dataflow) to normalize data from multiple sources. Prioritize data quality at ingestion—validate formats, remove duplicates, and standardize fields before they enter your warehouse.

Regulatory Compliance & Data Privacy

Fintech AI systems face dual compliance risk. First, they must comply with data privacy laws (GDPR, CCPA) governing how customer data is used in model training. Second, AI outputs—credit decisions, fraud flags—must be explainable to regulators.

Under GDPR Article 22, individuals have the right not to be subject to decisions based solely on automated processing that produce legal or similarly significant effects. CCPA regulations effective January 1, 2026 require risk assessments and cybersecurity audits for Automated Decisionmaking Technology.

Solutions include:

- Data anonymization for model training to protect customer privacy

- Model explainability frameworks (XAI) that document decision logic for auditors

- Partnering with SOC 2 certified vendors to ensure enterprise-grade security standards

- Regular compliance reviews as regulations evolve

Algorithmic Bias & Model Governance

AI models trained on historically biased financial data can perpetuate discriminatory outcomes, particularly in credit scoring and fraud detection. This carries both regulatory risk and reputational risk for neo banks.

The CFPB requires creditors to provide specific, accurate adverse action reasons. If a model is too complex to explain its decisions, it cannot legally be used for credit scoring under existing fair lending laws.

The solution involves:

- Regular bias audits across protected demographic groups to catch discriminatory patterns before they reach production

- Diverse training datasets that reflect your actual customer base, not just historical approval populations

- Human-in-the-loop review for high-stakes decisions like credit denials and fraud flags

- Explainable AI frameworks that log decision factors in language auditors and regulators can act on

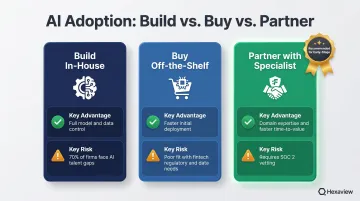

The Build vs. Buy vs. Partner Decision

This is the most consequential early decision for fintech AI adoption. Each path has real tradeoffs:

| Approach | Advantage | Key Risk |

|---|---|---|

| Build in-house | Full control over models and data | 70% of financial services firms report AI talent gaps, especially in technical, risk, and compliance roles |

| Buy off-the-shelf | Faster initial deployment | Generic platforms rarely adapt to fintech's regulatory requirements or custom data architectures |

| Partner with a specialist | Domain expertise + faster time-to-value | Requires vetting for security certifications (SOC 2 Type 2) and genuine fintech delivery experience |

For most early-stage fintechs, partnering bridges the gap — providing the ML engineering depth and regulatory familiarity that takes years to build internally, without committing to a full-time AI team before product-market fit is established.

How Hexaview Powers AI Transformation for FinTech Startups & Neo Banks

Hexaview Technologies holds SOC 2 Type 2 certification and AWS Select Tier Partner status, backed by over 10 years of capital markets and wealth management experience. Recognition on the WealthTech 100 and DATATECH50 lists reflects a track record built specifically around the security, compliance, and scalability demands fintech teams face.

Hexaview delivers end-to-end AI consulting and automation services for fintech clients:

- AI Engineering: Fraud detection systems built for a New York-based fintech client achieved 25% higher acceptance rates and 7% fraud reduction — covering everything from data strategy and ML model development through production deployment

- Agentforce-Powered Automation: Compliance-aware workflow automation that cut case handling time by 30% and reduced manual work by 45% for financial services clients

- Salesforce CRM Integration: Customer data unification connecting banking cores, payment processors, and third-party APIs through certified Ridge Consulting Partner expertise

A 200+ person team has served clients including LPL Financial and Addepar, operating across US and India delivery centers to move projects from scoping to production without handoff delays.

To assess your current data infrastructure and map out an AI adoption roadmap, reach out to the Hexaview team at hello@hexaviewtech.com or call +1 (845) 653 3855.

Frequently Asked Questions

How can AI be used in fintech startups?

AI can be applied across fraud detection, credit underwriting, customer onboarding, compliance automation, and personalized financial services. This lets startups automate high-cost, high-risk operations at scale and compete with far larger institutions.

What AI automation solutions are most critical for neo banks?

KYC/onboarding automation, 24/7 AI-powered customer support, real-time fraud detection, and intelligent back-office automation are the highest-priority areas. Neo banks operate without physical branches and must deliver seamless digital experiences at scale with lean teams.

What is the difference between AI consulting and AI development for fintech?

AI consulting covers strategy, use case prioritization, vendor selection, and roadmap planning. AI development involves building and deploying the actual models and systems. Hexaview delivers both as a single integrated engagement, so strategy and execution stay aligned throughout.

How do fintech startups ensure AI models comply with financial regulations?

Most compliance-ready AI programs rely on a few core practices:

- Explainable AI (XAI) frameworks to produce audit trails regulators can review

- Data anonymization and consent management for privacy compliance

- Regular bias audits to catch model drift or discriminatory outputs

- Vendors with certifications like SOC 2 Type 2 for security assurance

How long does it take to implement AI solutions in a fintech startup?

Implementation timelines vary by use case. A fraud detection MVP can often be deployed in 8-12 weeks; a full data platform with multiple AI models typically takes 6-12 months. Starting with a phased, use-case-first approach with an experienced partner cuts deployment time and delivers results faster.

What should a fintech startup look for in an AI consulting partner?

Evaluate proven fintech domain expertise, security certifications (SOC 2), a delivery track record with similar clients, cloud infrastructure partnerships (AWS/Azure), and the ability to provide both strategic guidance and hands-on engineering execution—not just one or the other.