Introduction

Hedge fund managers and wealth advisors face a risk environment that has grown structurally more complex. The VIX spiked to 2008-level extremes during March 2020, and global hedge fund AUM reached $4.9 trillion by Q3 2024 — an 8% year-over-year increase that directly amplifies exposure.

Alternative assets are proliferating across multi-strategy platforms, and regulators are tightening scrutiny with expanded Form PF requirements and quarterly 13G filings.

Legacy risk frameworks built on static VaR models and manual processes are structurally unable to keep pace. When the Basel Committee examined COVID-19 market dislocations, it found that traditional VaR frameworks produced widespread backtesting exceptions, with market risk capital requirements rising 20-25%.

Supervisors across multiple jurisdictions were forced to override model outputs — a direct signal that decades-old statistical approaches fail precisely when accurate risk signals matter most.

Multi-asset portfolios, cross-border exposures, and the pace at which market conditions shift demand a fundamentally different approach. This article examines how AI-powered risk analytics and automation are closing that gap for hedge funds and wealth management firms.

Key Takeaways

- AI replaces backward-looking VaR models with real-time predictive intelligence, reducing quantile loss by up to 27% versus traditional benchmarks

- Automation eliminates manual bottlenecks in trade surveillance, regulatory reporting, and portfolio monitoring — compliance costs have surged 60% since the financial crisis

- Use cases cover predictive market risk, counterparty assessment, fraud detection, and alternative data integration for early-warning signals

- Implementation hurdles around legacy integration, explainability, and governance are addressable through modular architecture, phased rollout, and structured governance frameworks

Why Traditional Risk Models Fall Short for Hedge Funds and Wealth Managers

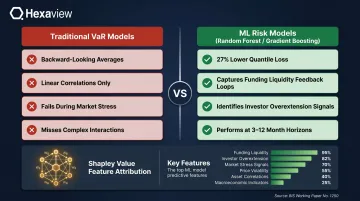

Legacy VaR Models Fail During Market Dislocations

Most legacy risk systems rely on historical Value-at-Risk (VaR) models and rule-based compliance engines that depend heavily on past data and linear correlations. These frameworks are structurally weak during non-linear market events — liquidity crises, flash crashes, or pandemic-driven volatility spikes.

The Basel Committee's post-COVID analysis documented this failure in detail. During March 2020, the S&P 500 fell 30% and implied volatility exceeded 2008 levels. Multiple banks experienced VaR backtesting exceptions, triggering automatic capital multiplier increases.

In some cases, the stress exceeded even the Stressed VaR (sVaR) calibration period — meaning "worst case" models still underestimated actual losses. Supervisors ultimately allowed banks to disregard backtesting exceptions, a tacit acknowledgment that traditional VaR is inherently procyclical and fails precisely when it's needed most.

The Manual Process Tax

Risk teams at hedge funds and wealth management firms spend disproportionate time aggregating data from disconnected systems rather than analyzing and acting on signals. Data flows from order management systems, custodians, prime brokers, and third-party vendors rarely conform to the same schema.

McKinsey research puts the cost in plain terms: knowledge workers lose approximately 1.8 hours per day — roughly 9 hours per week — searching for and gathering information. The Basel Committee's BCBS 239 framework confirms this pattern holds in financial services, where manual, judgment-based data aggregation remains widespread. That burden pulls skilled analysts away from interpretation and decision-making, the work that actually drives returns.

Growing Complexity Legacy Tools Cannot Handle

Data aggregation problems don't exist in isolation — they compound against a backdrop of structural complexity that legacy tools simply weren't designed to handle.

Multi-strategy hedge funds running equity long/short, macro, and credit strategies simultaneously need cross-asset risk aggregation that point-in-time VaR models cannot provide. These platforms must evaluate:

- Concentration risk across instruments that correlate differently under stress

- Hidden correlations between seemingly unrelated positions

- Tail-risk exposures that only surface in non-linear market conditions

Wealth managers face a different but equally pressing version of the same problem. Serving ultra-high-net-worth clients requires personalized, household-level risk views that reflect each client's goals, tax considerations, and liquidity needs. Spreadsheet-based processes cannot scale to that level of customization across hundreds or thousands of portfolios.

Key AI Risk Analytics Applications in Hedge Funds and Wealth Management

Predictive Market Risk Modeling

Machine learning models — particularly gradient boosting and deep learning architectures — analyze real-time price feeds, order book data, macro indicators, and cross-asset correlations to generate forward-looking risk estimates rather than backward-looking historical averages.

BIS Working Paper No. 1250 demonstrated that tree-based ML models significantly outperform traditional approaches:

- Random forests achieve up to 27% lower quantile loss than autoregressive benchmarks, especially at 3-12 month horizons for money market and FX stress prediction

- ML models capture complex interactions — such as feedback between dealer balance sheets and funding liquidity — that drive market stress

- Key predictive features identified via Shapley values: funding liquidity, investor overextension, and the global financial cycle

For hedge funds, the result is continuous multi-factor scenario analysis across the full portfolio — surfacing concentration risks, hidden correlations between seemingly unrelated positions, and tail-risk exposures that traditional VaR calculations miss.

A separate BIS study (Working Paper No. 1291) introduced a two-stage approach combining Recurrent Neural Networks with Large Language Models for market monitoring. The RNN produces interpretable daily forecasts of market dysfunction 60 business days ahead, consistently outperforming AR(1) baselines.

Counterparty and Credit Risk Assessment

AI evaluates counterparty risk in hedge fund contexts — prime broker exposure, OTC derivatives counterparties — by integrating market signals with financial statement data. Unlike quarterly credit reviews, AI models ingest CDS spreads, equity volatility, and news sentiment continuously to produce dynamic creditworthiness scores that update in real time.

For wealth management, AI models assess credit risk across client loan books — margin lending, collateral-backed lending — using alternative data inputs. Earlier signals mean more accurate risk-adjusted pricing before deterioration appears in traditional financial metrics.

Fraud Detection and Trade Surveillance

AI-powered trade surveillance systems analyze order patterns, communication metadata, and execution behaviors to detect market manipulation, insider trading signals, and unauthorized activity far faster than rule-based threshold alerts.

The FCA's Market Abuse Surveillance TechSprint (October 2024) brought together 200+ representatives to test AI/ML approaches against 1 TB of pseudonymized market data. Key techniques tested included:

- Isolation Forests to reduce false positives and improve alert accuracy

- Bayesian Network Analysis for identifying manipulation with limited data

- Econophysics models to detect subtle order book manipulation

- Large Language Models to contextualize outliers and filter false positives

- Parameter-free ML for auto-calibration to shifting market conditions

The TechSprint confirmed that AI/ML approaches identify complex abuse patterns — such as cross-market manipulation — that rules-based tools consistently miss.

Adaptive ML models learn evolving manipulation tactics rather than matching static rule sets, making them more resilient to sophisticated actors over time.

Alternative Data Integration for Risk Signals

AI enables hedge funds to ingest and process alternative data sources — satellite imagery, shipping data, social media sentiment, web scraping, earnings call transcripts — and translate them into risk-relevant signals.

Lowenstein Sandler's 2024 Alternative Data Survey found:

- 67% of investment management respondents now use alternative data, more than doubling from 31% in 2022

- 94% of current users plan to increase budgets allocated to alternative data

- The global alternative data market is estimated at over $9 billion

AI can detect supply chain stress in portfolio companies by analyzing shipping data or satellite imagery of facility parking lots weeks before that stress surfaces in quarterly financial statements — giving risk managers a measurable lead time on deteriorating fundamentals.

Automating Risk Operations for Investment Managers

Trade Surveillance Automation

AI-driven workflow engines monitor positions, exposures, and limit breaches in real time, automatically escalating alerts to the appropriate risk officer with contextual analysis appended. This replaces the manual monitoring cycle that typically runs on a T+1 or end-of-day basis.

AI models prioritize alerts based on historical patterns, market conditions, and portfolio context — filtering noise so risk officers spend time on genuine anomalies, not false positives.

Regulatory Reporting Automation

The same data flowing through surveillance systems feeds directly into a growing regulatory reporting burden. The Managed Funds Association formally urged the SEC and CFTC in December 2025 to rescind 2023 and 2024 Form PF amendments, characterizing them as "burdensome and duplicative." Quarterly Schedule 13G filings, AIFMD reporting, and MiFID II transaction reporting add layers of compliance complexity.

AI can extract, validate, and format required data from multiple source systems, reducing the reporting cycle from days to hours while minimizing human error. Automation pipelines handle reconciliation across OMS data, custodian records, and trade confirmations — freeing compliance teams to focus on exceptions and governance decisions.

Client Portfolio Risk Reporting for Wealth Managers

AI can auto-generate personalized, household-level risk reports for each client — showing exposure breakdowns, drawdown risk, and goal-based risk metrics — at a scale that would be impossible with manual analyst workflows.

Workflow Orchestration

Agentic AI can chain together tasks in a single automated workflow that previously required coordination across three or four teams:

- Flag a limit breach

- Pull relevant position data

- Run an impact scenario

- Draft a risk memo

- Notify stakeholders

Chaining these steps cuts response time from hours to minutes and enforces consistent escalation protocols — eliminating the coordination gaps that create regulatory and operational risk.

Hexaview Technologies has documented 20,000+ man hours saved in analysis for financial services clients through AI-driven workflow automation. The firm's SOC 2 Type 2 certified infrastructure meets institutional data security requirements, and its decade-plus of capital markets experience means models are built to satisfy both performance benchmarks and regulatory scrutiny.

AI-Driven Portfolio Risk Monitoring and Real-Time Stress Testing

Real-Time Risk Dashboards and Visualization

Modern AI platforms provide live portfolio risk dashboards that aggregate data across custodians, prime brokers, and internal systems. These dashboards show Greeks, factor exposures, liquidity profiles, and concentration metrics on a single pane of glass, updated continuously rather than at end-of-day.

For multi-strategy hedge funds, this means risk officers can monitor equity long/short, macro, and credit books simultaneously, with drill-down capabilities to individual positions and real-time P&L attribution.

Stress Testing and Scenario Analysis

AI dramatically expands the scope of stress testing. Instead of running a handful of pre-defined regulatory scenarios, ML models can simulate thousands of custom macro scenarios within minutes:

- Rate shock (sudden Fed policy change)

- Currency devaluation (emerging market crisis)

- Commodity spike (energy supply disruption)

- Geopolitical disruption (trade war escalation)

Each scenario computes impact on individual positions and the aggregate portfolio, allowing risk managers to identify vulnerabilities before they materialize. The Basel Committee's stress testing principles establish the regulatory foundation for this analysis, though they do not specify execution timeframes.

For wealth management, AI stress testing shows high-net-worth clients exactly how their portfolio would perform under scenarios personally meaningful to them, such as a recession scenario mapped to their retirement timeline. That specificity builds client trust in ways that generic VaR figures rarely achieve.

Drawdown Monitoring and Automated Rebalancing Triggers

AI monitors drawdown thresholds at both position and portfolio level in real time. When thresholds are breached, pre-approved workflows execute automatically:

- Notify portfolio managers when drawdown approaches threshold

- Reduce exposure in defined instruments automatically

- Activate hedges according to governance protocols

During rapid market dislocations — where prices can gap in minutes — automated response is the only practical defense. Manual escalation simply cannot match that speed.

Overcoming Implementation Challenges

Data Quality and Integration

The most common barrier is the fragmented data landscape. Prime broker feeds, custodian records, OMS data, and third-party market data rarely conform to the same schema. The FSB (October 2025) identifies model risk, data quality, and governance as sources of AI-related vulnerabilities that can pose risks to financial stability.

A robust data engineering layer must be established before AI models can produce reliable outputs:

- Data normalization to reconcile different vendor formats

- Entity resolution to match the same security across multiple data sources

- Unified risk data model that supports cross-asset aggregation

Firms with over a decade of capital markets experience, like Hexaview Technologies, bring the domain expertise needed to navigate the complexity of custodian feeds, prime broker APIs, and OMS integrations. That foundational data work is what determines whether downstream AI models produce reliable signals — or noise.

Model Explainability Requirements

Financial regulators and internal risk committees increasingly require that AI-driven risk decisions be interpretable and auditable. BIS FSI Occasional Paper No. 24 (September 2025) provides the most comprehensive survey of global explainability requirements:

| Regulator | Requirement |

|---|---|

| UK PRA (SS1/23) | Model risk management principles requiring explainability |

| IAIS | AI systems must produce "explainable, fair and unbiased" output |

| OSFI (Canada) | Validation must ensure models are "understandable to relevant stakeholders" |

| FINMA (Switzerland) | Assessed explainability "in greater depth" for investor-facing decisions |

| MAS (Singapore) | FEAT Principles plus thematic review of AI in financial services |

| EU | AI Act plus EBA guidance on ML for IRB models |

| US (FRB/OCC) | Business areas must be "able to question the model's assumptions" |

The IIF-EY (2025) reports that AI explainability is the top issue raised by financial institutions when engaging with regulators. A BoE/FCA (2024) survey found half of respondents had only partial understanding of their AI technologies due to third-party models.

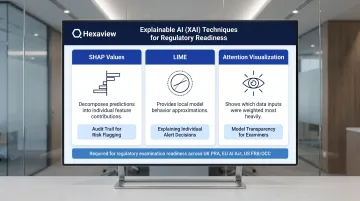

Explainable AI (XAI) techniques allow firms to understand why the model flagged a specific risk:

- SHAP values decompose predictions into individual feature contributions

- LIME provides local approximations of complex model behavior

- Attention visualization shows which data inputs the model weighted most heavily

These techniques are critical for regulatory examination readiness and internal governance — examiners expect a clear audit trail from input data to flagged risk.

Governance and Change Management

Successful AI risk programs require a governance framework that defines:

Model Validation Procedures:

- Independent validation team reviews model logic, assumptions, and performance

- Backtesting protocols compare model predictions to actual outcomes

- Documentation standards ensure reproducibility and auditability

Human Oversight Checkpoints:

- Define which decisions require human approval versus full automation

- Establish escalation protocols when AI flags high-severity risks

- Maintain override authority for portfolio managers and risk officers

Organizational Culture:

- Training programs to build trust in AI-generated signals

- Clear communication of model limitations and uncertainty ranges

- Incentive structures that reward appropriate use of AI insights

The IOSCO FR06/2021 report issued six specific guidance measures for firms using AI/ML, including requirements for appropriate governance, adequate testing, transparency, and human oversight.

Frequently Asked Questions

How is AI-driven risk analytics used in BFSI?

AI-driven risk analytics in BFSI applies ML, NLP, and predictive modeling to assess market risk, credit risk, fraud, and compliance risk in real time — replacing periodic, backward-looking analysis with continuous, forward-looking intelligence. Applications include trade surveillance, counterparty scoring, and scenario analysis.

Can AI do risk analysis in BFSI?

Yes. AI performs risk analysis across all major BFSI categories — market, credit, operational, liquidity, and compliance — with greater speed and accuracy than traditional rule-based models. It also handles multi-asset portfolios and non-linear market dynamics that legacy VaR frameworks cannot capture.

What are the types of AI risk in BFSI?

AI addresses traditional risk categories in BFSI — market, credit, operational, and fraud — using ML models. It also introduces new risks that firms must govern: model bias, explainability gaps, data privacy exposure, and adversarial attacks on AI systems.

What are the biggest challenges of implementing AI risk management in hedge funds?

Key implementation challenges include:

- Fragmented data infrastructure and legacy system integration

- Meeting model explainability requirements for regulators and risk committees

- Building governance frameworks that let teams trust and act on AI-generated signals

Data quality issues and vendor concentration add further systemic risk.

How does AI automation reduce operational costs in wealth management?

AI automation cuts costs by eliminating manual data aggregation, automating regulatory reporting, and generating client risk reports at scale. Smaller teams can manage larger, more complex portfolios without proportional headcount growth — a meaningful offset given that compliance costs have risen roughly 60% since the financial crisis.