Introduction

Wealth management firms and fund administrators face a punishing operational reality. The average relationship manager spends 60% to 70% of their time on non-revenue activities — wrestling with legacy systems and spreadsheets instead of serving clients. Operational teams dedicate 30% to 40% of their time to manual reconciliation and error correction.

That drain comes from disconnected technology stacks. Custodians, portfolio management platforms, CRM tools, reporting engines, and transfer agents all generate data in incompatible formats — and no one system speaks to another.

The result? Reconciliation breaks, delayed NAV calculations, T+1 reporting failures, and clients who expect real-time portfolio access but receive month-old statements.

This article covers what you need to know to fix that:

- Why API integration has moved from optional to essential for wealth managers and fund admins

- Which integration types deliver the most measurable value

- How to implement them using a phased framework

- Compliance considerations that cannot be skipped

Key Takeaways

- Disconnected systems consume over 50% of relationship manager time on manual tasks

- API integrations connect custodians, PMS platforms, CRM systems, and market data feeds, replacing error-prone manual processes

- Fund admins gain automated NAV workflows, real-time investor reporting, and tri-party reconciliation

- Successful implementations follow a three-phase approach: architecture assessment, phased build with validation, and continuous monitoring

The Fragmented Tech Stack: Why Wealth Management Needs Smarter Integration

Wealth management and fund administration technology stacks are built in layers — custodians feed position data up to portfolio management systems, which connect to trading desks, performance reporting tools, CRM platforms, and client portals.

Each layer was built a decade apart, with no native way to communicate with the others. The result is a fragmented environment where data moves slowly, breaks often, and costs firms more than most realize.

The Aggregation Nightmare

Data arrives from dozens of sources in wildly inconsistent formats. Major custodians like BNY Mellon, State Street, Fidelity, and Schwab each maintain proprietary API formats or SFTP-based feeds. Some still use SWIFT messaging for securities settlement. Others deliver CSV files. A few require manual downloads from secure portals. Investment managers receive FIX protocol messages for trade confirmations while fund accountants get proprietary XML feeds.

Operations teams spend hours normalizing this chaos before the data becomes usable for reporting or decision-making. More than one-third of financial services firms cite insufficient data infrastructure and legacy systems as the biggest barrier to digital transformation.

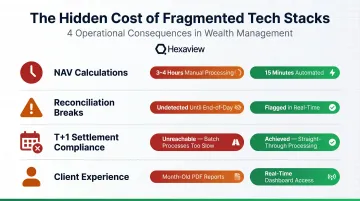

The Cost of Fragmentation

The operational consequences show up across the entire workflow:

- NAV calculations that take 3-4 hours manually complete in 15 minutes with API-driven systems

- Reconciliation breaks between custodian feeds, fund accounting, and investment manager records go undetected until end-of-day — triggering fire drills before market open

- T+1 settlement is unreachable for firms still running overnight batch processes; compressed cycles demand real-time data flows

- Client experience gaps widen when investors used to Robinhood or Coinbase receive month-old PDF statements via email

Legacy System Inertia

Many established wealth management firms operate on-premise systems or decade-old middleware never designed for modern API connectivity. 97% of fund groups still rely on spreadsheet tools for valuation tasks. This creates both technical debt and integration risk when modernizing.

43% of firms now acknowledge they need an entirely new technology stack to thrive in the age of AI and real-time client expectations.

That inertia doesn't exist in a vacuum — external forces are accelerating the pressure to change.

Forces Demanding Change

Three pressures are forcing integration modernization:

- Regulatory evolution: The SEC and CFTC continue modernizing reporting frameworks, while open finance regulations in Europe establish new data access rights. Firms need API infrastructure to absorb rule changes without manual rework each cycle.

- Client expectations: High-net-worth clients and institutional LPs expect secure mobile access to positions, performance, documents, and tax reporting — the same experience consumer fintech delivers.

- Competitive pressure: Tech-native RIAs and digital asset managers built on API-first architectures from day one. They operate with 40-60% lower middle-office costs and deliver client experiences traditional firms struggle to match.

Key API Integration Types for Wealth Management Platforms

Custodian and Prime Broker Data Feeds

Custodian integrations form the foundation. These APIs provide real-time or end-of-day position data, transaction histories, cash balances, and corporate action notifications directly into portfolio management or fund accounting systems.

The challenge? Each major custodian maintains its own format. Schwab's OpenView Gateway offers REST APIs and daily data files. State Street's Alpha Platform delivers real-time IBOR data through public APIs and Snowflake integration. J.P. Morgan's Fusion uses RESTful APIs with Python SDK support. Fidelity's Integration Xchange provides an open-architecture integration platform for clearing clients.

Firms managing assets across multiple custodians must build normalization logic for each feed — mapping disparate field names, date formats, and security identifiers to a common schema.

Portfolio Management System (PMS) Integration

PMS platforms like SS&C Advent Geneva, Orion, Black Diamond, or Addepar act as the operational data hub. API integrations connecting the PMS in both directions with trading platforms, risk engines, and reporting tools eliminate manual export-import cycles that introduce errors and delays.

Real-time data flow between the PMS and performance attribution engines ensures accurate client reporting without overnight batch reconciliation. When portfolio managers execute trades, the integration immediately updates client positions and performance metrics rather than waiting for the next morning's data refresh.

CRM and Client Portal APIs

Integrating CRM systems — Salesforce dominates wealth management — with portfolio and transaction data gives relationship managers a single interface showing positions, performance, pending transactions, and communication history. That consolidation removes the context-switching that slows client service.

This integration also powers personalized client portals where investors view holdings in real time, download statements, and submit service requests. Firms implementing Salesforce integrations for wealth management typically rely on specialized financial data flow configurations to connect CRM workflows to custodian and PMS data without building custom connectors from scratch.

Market Data, Reference Data, and Compliance Feeds

Market data APIs from Bloomberg, FactSet, or Refinitiv provide the pricing and index data needed for performance measurement, risk calculation, and regulatory valuation. Each feed type serves a distinct purpose:

- Real-time pricing — intraday quotes and NAV calculations for active portfolios

- Security master data — ISIN, CUSIP, and issuer details that maintain consistency across systems

- Benchmark indices — performance attribution and compliance reporting against mandated benchmarks

Without automated reference data feeds, security master mismatches accumulate quickly — and each mismatch becomes a potential reconciliation break that operations teams must chase down manually.

Fund Administration API Use Cases: Where Integration Delivers the Most Value

Not every integration point delivers equal return. These four workflows consistently produce the most measurable impact for fund administrators building API-connected operations.

NAV automation: API-driven workflows connect fund accounting systems directly to custodian position feeds and pricing data. This eliminates manual price entry and cuts NAV calculation cycles from 3-4 hours to near-real-time — a requirement for interval funds calculating daily NAV or ETFs needing intraday transparency.

Investor reporting portals: LPs increasingly expect self-service access to capital statements, performance reports, and tax documents. APIs feeding live data from fund accounting to investor portals eliminate manual intervention, reducing inbound service requests and differentiating fund admins competing for mandates.

Regulatory reporting automation: Fund administrators file across multiple regimes — Form PF, AIFMD Annex IV, FATCA/CRS, Form ADV. APIs connecting fund accounting and compliance systems to regulatory reporting platforms automate data extraction and reduce filing errors. The AIMA/KPMG compliance survey found compliance costs fall disproportionately on smaller firms, creating real market-entry barriers; automation directly reduces that burden.

Tri-party reconciliation: Daily reconciliation between fund administrator records, custodian records, and investment manager books is time-intensive and error-prone. API-based workflows surface breaks in near-real time rather than at end-of-day, cutting operational risk from discrepancies that would otherwise go undetected for hours.

A Framework for Platform Implementation in Wealth Management

Most implementation failures in wealth management don't happen during build — they happen before a single line of code is written. This three-phase framework addresses each stage: design, delivery, and ongoing operation.

Phase 1: Assessment and Architecture

Map your current system topology — every data source, target system, and data flow. Evaluate whether direct point-to-point integrations or an API gateway/middleware layer suits your scale. Define data governance standards: field mapping, normalization rules, master data ownership.

Key decisions:

- Which custodian feeds are highest volume and highest priority?

- Does your PMS support bidirectional APIs or only batch exports?

- Where will you enforce data validation — at source, in middleware, or at destination?

- Who owns the security master — custodian, PMS, or a separate MDM system?

Rushing to code without clear architecture leads to brittle point-to-point connections that break when any upstream system changes — and rebuilding those connections under production pressure costs far more than the planning phase ever would.

Phase 2: Build, Test, and Validate

Use sandbox or UAT environments mirroring production data. Start with the highest-volume, highest-value flows — typically custodian feeds and NAV calculations. Run parallel validation periods where API-driven outputs are reconciled against existing manual processes before cutover.

Firms that have worked across the full capital markets stack — including wealth platforms like LPL Financial and portfolio analytics tools like Addepar — already understand where reconciliation breaks typically occur. That pattern recognition shortens validation cycles and reduces the risk of production incidents at go-live.

Typical build sequence:

- Custodian position feeds → PMS (daily reconciliation)

- Market data pricing → fund accounting (NAV automation)

- PMS performance data → CRM (advisor dashboards)

- Fund accounting → investor portal (LP reporting)

- Compliance data → regulatory filing platforms (Form PF, AIFMD)

Phase 3: Operate, Monitor, and Evolve

API integrations require ongoing stewardship. Custodians update feed formats, regulators revise schemas, and new platforms get onboarded — often on short timelines with limited notice.

Essential practices:

- API monitoring: Track uptime, latency, error rates, and data completeness for every integration endpoint

- Versioning strategies: Maintain backward compatibility when upgrading APIs or changing data schemas

- Change management: Document every upstream provider update and test downstream impacts before production deployment

- Break resolution workflows: Automated alerts when reconciliation tolerances are breached, with documented escalation paths

Security, Compliance, and Data Governance in Financial API Integration

Authentication and Access Control

Financial API integrations in wealth management demand access controls that go well beyond standard web application security. Every system boundary — between portfolio management platforms, custodians, and reporting tools — is a potential exposure point for sensitive investor data and AUM records.

Authentication architecture typically includes:

- OAuth 2.0 for consumer-permissioned data access and machine-to-machine authentication flows

- Mutual TLS (mTLS) providing certificate-based client verification with encrypted transport

- API gateway centralization to enforce consistent security policies across all endpoints

- Zero-trust network principles for any system touching investor PII or fund-level data

Technology partners must demonstrate SOC 2 Type 2 compliance — evidence that security controls have operated effectively over time, not just passed a point-in-time audit. Hexaview holds SOC 2 Type 2 certification, which directly informs how integration architecture is designed and validated for wealth management clients.

Regulatory Compliance Obligations

Fund administrators serving cross-border or multi-jurisdiction structures face regulatory requirements that directly shape API design decisions — not just security posture. Getting this wrong creates examination risk, not just technical debt.

Key compliance considerations for API design:

- Data residency rules for cross-border fund structures (field-level controls on where data lands)

- Audit trail and data lineage requirements under SEC and FINRA guidance on third-party provider risks

- GDPR cross-border transfer safeguards for European investor data, with penalties up to €20 million or 4% of global turnover

- Data minimization — API calls should extract only the fields a given use case requires, nothing more

Data Governance Practices

Governance controls protect data integrity across the full integration lifecycle — from ingestion through transformation to downstream consumption. Without clear classification and access policies, custodian feeds and investor PII can end up handled inconsistently across systems.

Standard practices for financial data governance include:

- Field-level encryption for investor PII and financial account records at rest and in transit

- Tokenization of account identifiers when data crosses system or organizational boundaries

- Data classification policies defining how custodian feeds, NAV data, and PII are stored and shared within integration architecture

- Access logging with immutable audit trails to support regulatory examination and internal controls

Frequently Asked Questions

What is an API in fintech?

An API (Application Programming Interface) is a set of protocols enabling different financial software systems to communicate and exchange data securely. APIs power use cases from bank account connectivity to real-time portfolio reporting, replacing manual file transfers with automated data flows.

What are examples of API integrations?

Wealth management examples include:

- Custodian data feeds pulling real-time positions into a portfolio management system (PMS)

- Salesforce CRM connected to portfolio performance data for relationship manager dashboards

- Fund accounting systems feeding automated investor reporting portals with live capital account balances

What are the 4 types of REST API?

REST APIs use four core HTTP methods. In financial contexts:

| Method | Action | Wealth Management Example |

|---|---|---|

| GET | Retrieve data | Fetch current portfolio positions |

| POST | Create data | Submit a trade instruction |

| PUT/PATCH | Update data | Modify client profile information |

| DELETE | Remove data | Remove an outdated account record |

What are the biggest risks in a wealth management API integration?

The most common failure points are data mapping mismatches between source and target systems, custodian API rate limits that break overnight batch processes, and insufficient error-handling logic that causes silent data gaps. Firms that document field-level data dictionaries before development begins avoid most of these issues.

How long does it typically take to implement a wealth management platform integration?

Timeline varies significantly by complexity. A single custodian feed integration typically takes 4-8 weeks. Full multi-system implementations spanning PMS, CRM, reporting, and regulatory filing can take 6-18 months. The most common cause of delays is skipping the data governance and field-mapping phase — firms that lock down their architecture before writing code consistently hit earlier go-live dates.